February 13, 2026

Technology stocks have surged since the AI boom, driving valuations higher and embedding lofty earnings expectations, leaving little room for error and fueling recent market volatility.

Investor nervousness has led to sharp, sometimes indiscriminate reactions—punishing software stocks amid fears that AI models like Claude will upend the industry—while hardware stocks like semi- conductors have rallied strongly, creating an unprecedented performance gap.

The pessimism toward software may be overdone. AI is fundamentally software at its core and is more likely to transform and enhance the industry rather than replace it, suggesting that the current divergence between hardware and software could normalize over time.

Many of us are familiar with the children’s game of Hot Potato, we may have even played it as kids ourselves. The premise of the game is simple, players pass around an object, and the goal is to avoid being the person left holding said object when the music stops; fail and you are out of the game. Frankly, I was never a big fan of the game myself. I often thought that if there was nothing wrong with the proverbial “potato”, even if nobody wanted it, why would I not just keep it for myself? I get it, it was a game, but I must admit that the thought crossed my mind as a child. However, the market recently has not appeared to share my opinion on the subject.

It is a known fact that, since the beginning of the artificial Intelligence boom in late 2022, stocks in the Technology sector have moved meaningfully higher, regardless of industry. As the sector moved higher, valuations moved higher along with it. On a trailing P/E basis, the S&P 500 Information Technology sector is currently trading near 35x trailing earnings, creeping closer and closer to its 10-year high of

38.5x. However, by definition, trailing earnings is a backward-looking metric, basing itself on earnings over the past twelve months. What about future earnings, which the market expects to see going forward? This is where forward-earnings come in, a metric based on looking ahead at the coming twelve months. On a forward-earnings basis, the Information Technology sector is currently trading with a P/E of 25x earnings. So, if we do the math, if the P/E based on trailing earnings is 35x, and the P/E based on forward earnings is 25x, that means that the E in the formula is expected to meaningfully rise over the next twelve months to make the overall P/E lower. Said a different way, the market has very high expectations for earnings growth in the Information Technology sector in 2026. In fact, according to data compiled by FactSet, coming into the year, the market was expecting 28% earnings growth in the Information Technology sector for the year head. Those are very lofty numbers for this sector, considering that the expected average earnings growth for the entire S&P 500 is 15%. Such high expectations leave very little room for error, a backdrop that provides some context for the current jitters being felt by inves- tors across the Technology sector.

To be fair, investors in this sector were already feeling nervous towards the end of last year. After peaking in late October, the Nasdaq Composite proceeded close to 10% lower over the following month, after Meta reported the need to issue debt to fund its AI spending plans. This announcement led to heavy scrutiny by investors as to which companies could potentially be stretching their balance sheets beyond their limits to fuel capex plans. The balance sheets of companies like Meta, Oracle, and CoreWeave were put under the micro- scope, while their stocks saw meaningful pullbacks. Gripped by panic, something that the market appeared to overlook was the fact that unlike some of its hyperscaler brethren such as Microsoft and Amazon, that generate high levels of cash flow from their cloud businesses, Meta does not have a cloud business to act as a cash flow machine. As such, the company must find other avenues to fund its capex plans; simply put, whether it is through debt, equity issuance, or other means, it has to generate the funds needed to spend in order to grow, it is the business model of most technology-oriented companies. Interestingly, the market seemed to finally come to grips with this realization, evidenced by the fact that during its most recent earnings report at the end of last month, even though Meta reported capex numbers that were even higher than those reported in the previous quarter, the stock closed 11% higher on the day. Although the stock’s reaction seems counterintuitive, the market had had time to take a breath and digest Meta’s situation over the time between earnings reports, realizing that Meta is not Microsoft or Amazon. All stocks, even if they are in the same industry, cannot be painted with the same brush. However, like a nervous cat that jumps two feet in the air when it hears thunder, a nervous Wall Street sometimes also tends to react first and ask questions later.

A jittery market tasked with beating seemingly high expectations will jump at anything. A more recent example of this behavior was the pullback that tech- nology stocks experienced over the last few weeks, unraveled by Microsoft’s quarterly earnings report at the end of January. Microsoft reported earnings that beat Wall Street’s expectations; however, good was not good enough. The Street focused instead on the fact that like most of its hyperscaler peers, Microsoft reported higher than expected capex, while at the same time, its cloud business, Azure, saw a slight decrease in growth. The stock closed 10% lower on the day. Google and Amazon followed, both reporting numbers that would have been great in any other context, but not in one with high expec- tations and little room for error. Six months ago, these were the companies that could do no wrong, now they are getting punished because they are not good enough.

Enter Claude. Claude is an advanced suite of artifi- cial intelligence models developed by Anthropic, which can tackle numerous tasks such as under- standing, analyzing, and creating text, content, and code. One of the most distinctive features of Claude is that it can reason, analyze, and solve problems with almost human-like qualities. Claude’s advent unleashed in the market an AI-driven temper tantrum of sorts, much like when China’s DeepSeek AI large language model (LLM) entered the scene early last year. Just as the market began to price in every other LLM’s demise at the hands of DeepSeek, it now seems to be pricing in the demise of software, especially the Software as a Service (SaaS) business model, at the hands of Claude. Companies in indus- tries as diverse as the legal and financial fields, where the market is speculating that Claude will replace some of the products and services they provide, have seen their stocks drop 25%, on average, over the past few weeks. On the other side of the coin, however, is hardware. The market is currently assigning a steep premium to hardware companies, implying that, whatever chaos AI unleashes on the software industry, this new technology will still require hardware such as chips and semiconductors.

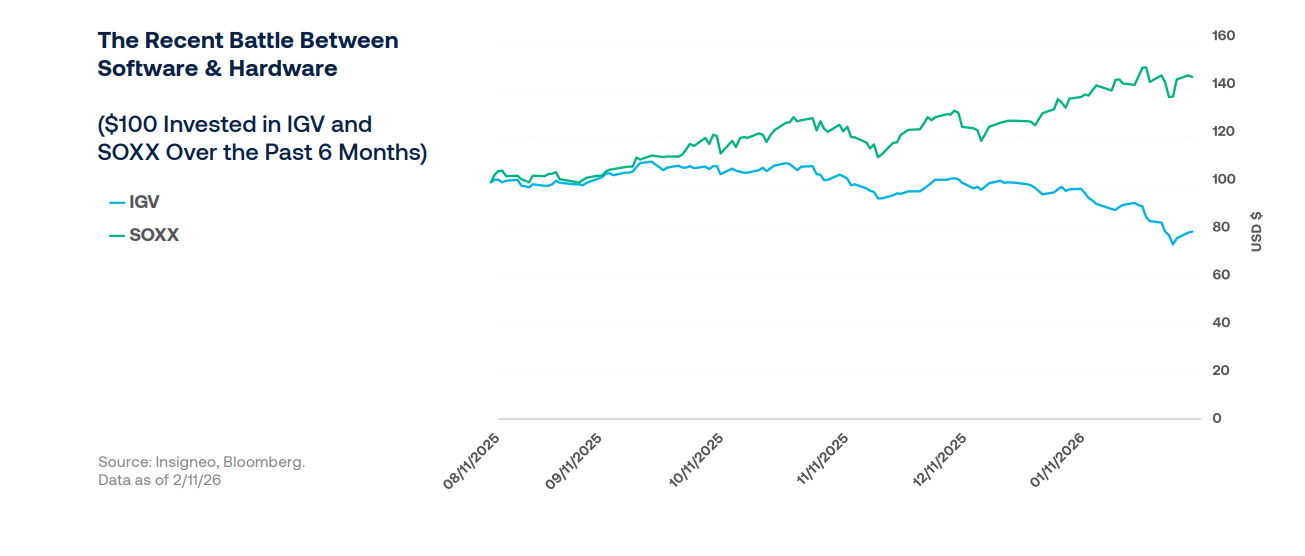

The chart below depicts the recent battle between software and hardware. As we can see from the chart, $100 invested six months ago in the computer hardware industry, represented by the iShares Semiconductor ETF (SOXX), would have grown to

$145, as of the time of this writing. On the other hand, the same $100 invested six months ago in the computer software industry, represented by the iShares Expanded-Tech Software Sector ETF (IGV), would have shrank to approximately $80, losing $20 in value. A spread this wide, in the range of 65%, between two traditionally complementary indus- tries in the Information Technology sector has never been seen before. Keep in mind that most of this discrepancy has occurred over a period of merely six months.

We believe that the current sentiment towards the software sector is overly negative, exacerbated by existing market nervousness propagated by seem- ingly unreasonable expectations. The problem that we see with the market’s overly pessimistic stance towards software is that, at the end of the day, arti- ficial intelligence is also software. As such, the logic that AI alone will obviate the current software industry, and that it alone will fill the demand for hardware, appears incongruent. Hardware and software are complementary industries, not mutually exclusive, and like it or not, AI is software at its core.

The difference is that AI is probabilistically based software, meaning that it can adapt and learn as it goes, whereas most software as we know it is deterministic, meaning that it must be prepro- grammed. As such, AI is likely to build on and enhance software as we know it, not eradicate it.

Given an already jittery environment though, inves- tors have been selling most software-related stocks indiscriminately, passing on the proverbial “hot potato” that no one wants to be holding when AI turns off the music. But what if AI does not turn off the music, simply changes the tune? As Barclay’s commented in a recent report, “software is not dead, it is just changing”. We believe that this encapsulates what will most likely prove to be the case over time. Additionally, AI will not impact all software players equally. Large, established players such as Microsoft, SAP, Palantir, Snowflake, and Salesforce, among others, are unlikely to just throw their arms up in the air and give up. They are more likely to adapt and grow with AI, offering enhanced products and services. In fact, we have seen this dynamic play out many times over industry and technology cycles, where, although some players inevitably disappear and give way to new players entering the industry, entrenched players adapt and become stronger. Microsoft is actually a great example of a company that has been able to adapt over many cycles; just think of how far the company has come since offering its flagship Windows 95 software on large, clunky computers.

With history as our guide, we believe that the wide discrepancy between both software and hardware industries will likely be resolved over time. This does not mean that both industries will not remain volatile in the near future. In fact, as of the time of this writing, there are still stocks being heavily penalized by the fear of being replaced by AI. However, over the long term, once the dust settles and Wall Street can take a deep breath and evaluate the situation from a more rational standpoint, both software and hardware industries are likely to revert back to their respective means. With this in mind, investors with the appropriate risk tolerance and investment horizon could be well served to begin evaluating whether they too should pass on the proverbial “hot potato” that Wall Street is passing around, or stop to examine it in more detail; after all, it may be worth keeping it for themselves.

It is important to keep in mind that the individual equities referenced here can exhibit high degrees of volatility and are not suitable for every investor. These investments are best considered on a case- by-case basis, based on a particular investor’s will- ingness and ability to tolerate risk. Please consult with your financial advisor prior to pursuing invest- ments in any of the companies mentioned above.

The difference is that AI is probabilistically based software, meaning that it can adapt and learn as it goes, whereas most software as we know it is deterministic, meaning that it must be prepro- grammed. As such, AI is likely to build on and enhance software as we know it, not eradicate it.

Given an already jittery environment though, inves- tors have been selling most software-related stocks indiscriminately, passing on the proverbial “hot potato” that no one wants to be holding when AI turns off the music. But what if AI does not turn off the music, simply changes the tune? As Barclay’s commented in a recent report, “software is not dead, it is just changing”. We believe that this encapsulates what will most likely prove to be the case over time. Additionally, AI will not impact all software players equally. Large, established players such as Microsoft, SAP, Palantir, Snowflake, and Salesforce, among others, are unlikely to just throw their arms up in the air and give up. They are more likely to adapt and grow with AI, offering enhanced products and services. In fact, we have seen this dynamic play out many times over industry and technology cycles, where, although some players inevitably disappear and give way to new players entering the industry, entrenched players adapt and become stronger. Microsoft is actually a great example of a company that has been able to adapt over many cycles; just think of how far the company has come since offering its flagship Windows 95 software on large, clunky computers.

With history as our guide, we believe that the wide discrepancy between both software and hardware industries will likely be resolved over time. This does not mean that both industries will not remain volatile in the near future. In fact, as of the time of this writing, there are still stocks being heavily penalized by the fear of being replaced by AI. However, over the long term, once the dust settles and Wall Street can take a deep breath and evaluate the situation from a more rational standpoint, both software and hardware industries are likely to revert back to their respective means. With this in mind, investors with the appropriate risk tolerance and investment horizon could be well served to begin evaluating whether they too should pass on the proverbial “hot potato” that Wall Street is passing around, or stop to examine it in more detail; after all, it may be worth keeping it for themselves.

It is important to keep in mind that the individual equities referenced here can exhibit high degrees of volatility and are not suitable for every investor. These investments are best considered on a case- by-case basis, based on a particular investor’s will- ingness and ability to tolerate risk. Please consult with your financial advisor prior to pursuing invest- ments in any of the companies mentioned above.

Insigneo Financial Group, LLC comprises a number of operating businesses engaged in the offering of brokerage and advisory products and services in various jurisdictions. Brokerage products and services are offered through Insigneo Securities, LLC, a broker-dealer registered with the U.S. Securities and Exchange Commission (“SEC”) and member of FINRA and SIPC. Investment advisory products and services are offered through Insigneo Advisory Services, LLC, an investment adviser registered with the SEC. Insigneo has affiliated companies in different locations, so it is important to understand which entity you are conducting business with. Please visit https://insigneo.com/legalentities/ for more information about the differences between these companies, their locations, and what that means for you.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security. It is for general information purposes only. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security. It does not constitute a recommendation or a statement of opinion, or a report of either of those things and does not, and is not intended, to consider the particular investment objectives, financial conditions, or needs of individual investors. Any target prices provide reflect our current expectations, are subject to change and may not be achieved due to a variety of risks, including changes in economic conditions, interest rates, geopolitical developments, and issuer-specific factors. The target price does not guarantee future results and should not be relied upon as a sole basis for investment decisions.

Not All Risks Are Disclosed – Past performance is not indicative of futures results. Investments involve significant risks, and it is possible to lose some or all of your principal investments and therefore may not be suitable for everyone. Always consider whether any investment is suitable for your particular circumstances and, if necessary, seek professional advice from your Investment Professional. This material may contain opinions, expressions, and estimates that represent the analysis and perspective of Insigneo Securities, LLC’s Investment Strategy department or its providers at the time of publication. These are subject to change at any time, without notice.

Insigneo Asesorías Financieras SPA se encuentra inscrito en Chile, en el Registro de Prestadores de Servicios Financieros de la Comisión para el Mercado Financiero. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de emisión de este. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera.

Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Asesorías Financieras SPA ni ninguna de sus empresas relacionadas.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta o solicitud de compra o venta de ningún valor en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en cuentas de corretaje y de asesoramiento de inversiones están sujetas al riesgo de mercado, incluida la pérdida de capital.

La información base del presente informe puede sufrir cambios, no teniendo Insigneo Securities LLC ni Insigneo Asesorías Financieras SPA la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.

Insigneo Asesor Uruguay S.A. está inscripto en el Registro de Mercado de Valores del Banco Central del Uruguay como Asesor de Inversiones. En Uruguay, los valores están siendo ofrecidos en forma privada de acuerdo al artículo 2 de la ley 18.627 y sus modificaciones. Los valores no han sido ni serán registrados ante el Banco Central del Uruguay para oferta pública. Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted según su perfil y estrategia de inversión. Este documento no constituye un asesoramiento ni una recomendación u oferta o solicitud de compra o. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso. Rentabilidades históricas de los productos anunciados no aseguran rentabilidades futuras..

Insigneo Argentina S.A.U. Agente Asesor Global de Inversión se encuentra registrado bajo el N° 1053 de la Comisión Nacional de Valores (CNV) e inscripto ante la Inspección General de Justicia (IGJ) bajo el N° 12.278 del Libro 90, Tomo –, de Sociedades por Acciones. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de su emisión. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera. Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Argentina S.A.U. ni ninguna de sus empresas relacionadas. La información base del presente informe puede sufrir cambios, no teniendo Insigneo Argentina S.A.U. la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta, recomendación o solicitud de compra o venta de ningún valor negociable en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.