January 16, 2026

U.S. equities ended 2025 with solid gains led by large-cap tech, but looking ahead to 2026 the rally is expected to continue with broader market participation, as earnings growth could become less concentrated in a handful of technology stocks.

While large-cap tech should continue to grow, its dominance is likely to normalize, with small caps and sectors such as Industrials, Healthcare, Financials, Utilities, Energy, Materials, and select Consumer Discretionary areas contributing more meaningfully as market breadth widens.

Our year-end S&P 500 target of 7,600 is based on 12–13% earnings growth and sector rotation; however, investors should remain balanced and vigilant given risks from various factors such as geopolitics, inflation, interest-rate paths, labor markets, and political uncertainty. In this two-part series, we will delve into our outlook for global equity markets. Starting with U.S. equity markets, we will explore what could be in store for equities in 2026, including potential opportunities, as well as risks.

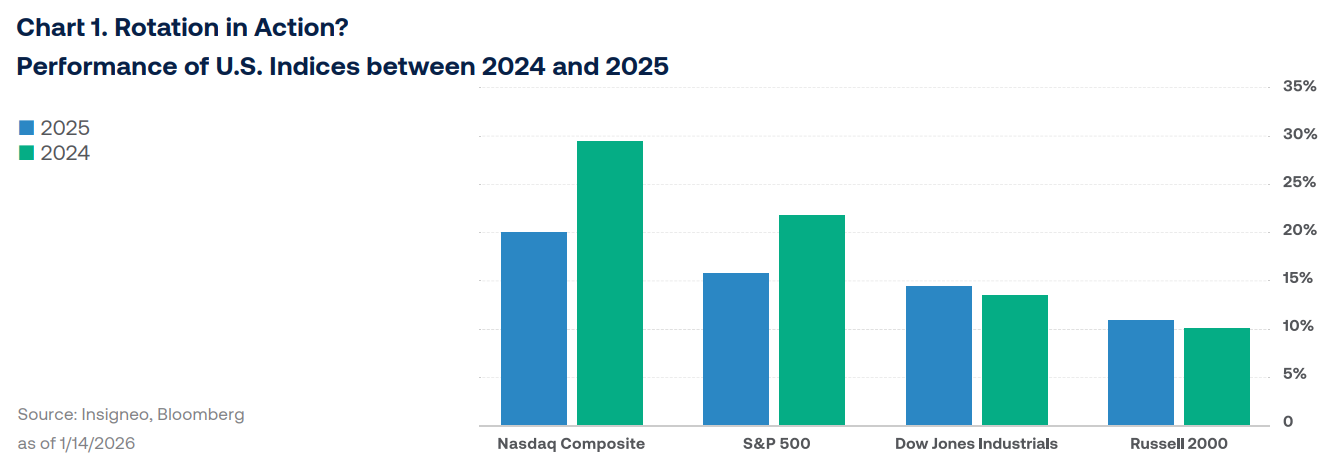

U.S. equity markets closed 2025 with a bang. The Nasdaq Composite led the pack, closing the year 20.4% higher, followed by the S&P 500, Dow Jones Industrials, and Russell 2000, which rose 16.4%, 13%, and 11.3% respectively. It was a great year to be invested in U.S. equities. Naturally, the question arises: Could the rally that began in 2023 continue in 2026? In short, we think so, but the market leaders could be different, or at least more diversified. What do we mean by that? For starters, we all know that large cap technology firms have been the leaders of this rally, mostly driven by the advent of artificial intelligence. Going forward, we believe that, although large cap technology firms will continue to see earnings growth in 2026 and still be meaningful players in the market’s march higher, earnings growth will not be as heavily concentrated in a handful of stocks. In other words, other sectors of the economy will likely contribute more to overall earnings growth than in past years.

In previous writings, we have said that for the market to keep marching higher in a healthy manner, market breadth needed to expand. As a refresher, market

breadth is the number of companies or sectors participating in an equity market’s directional trend. More companies and sectors participating in an up-trending market means wider market breadth and a healthier rally. In this context, it is important to remember that sustainable markets trends are underpinned by healthy earnings growth, not just P/E multiple expansion. Data compiled by Capital Economics showed that since the end of 2022, approximately 70% of the S&P 500’s earnings have mostly stemmed from the large-cap technology complex. In fact, a recent study by Black Rock revealed that if we removed the earnings contribution of the Magnificent Seven stocks from the S&P 500 over a similar period, we would have experienced at least one quarter of negative earnings growth. Although this data may appear outlandish, it is not uncommon, as the sectors that are initially responsible for the birth of new technologies tend to be the ones that initially benefit the most. However, based on the theory that healthy equity rallies are supported by wide market breadth, these data underscore the fact that for the current rally to continue, the over-concentration of earnings growth has to decrease and expand into more areas of the economy. To this point, since mid-last year we have been calling for a “rotation” of equity outperformance, away from just the large-cap technology complex, to include other parts and sectors of the markets.

Mind you, this does not mean that large-cap technology is going to underperform. It just means that earnings growth from these companies should begin to normalize; still growing, but maybe at slightly lower rates than in previous years, while other parts of the market begin to play catch up as they see their own earnings begin to move higher. We believe that we started to see this dynamic last year. Chart 1 shows the performance of U.S. indices between 2024 and 2025. We can see that in 2024, the large cap tech-heavy Nasdaq Composite and S&P 500 meaningfully outperformed compared to 2025, while the more value and cyclically oriented Dow Jones Industrials and Russell 2000 indices posted weaker returns that year versus 2025. In other words, the performance of large cap technology-heavy indices, although strong, was not as strong in 2025 as it was in the previous year, while value and cyclically oriented indices performed better in 2025 than the previous year. Curiously, if we were to include 2023 performance on the graph, we would see that, although the Nasdaq Composite was up 29% in 2024, that number was lower than the 43% move it posted in 2023! This trend makes sense, as the sectors initially responsible for new technologies gradually give way to other sectors, assuming a favorable economic backdrop. We think that we will continue to see this rotation in 2026.

What does this mean in terms of equity strategy for the year ahead? First and foremost, balance will be key. As we can see on the graph, although leadership

rotation is likely to continue, this does not mean that we think that large cap tech is going to underperform, just that returns might not be as abnormally

high as seen over the last three years. Said in a different way, we are by no means encouraging investors to eliminate their exposure to large cap tech, we are simply saying that investors with outsized positions in this segment of the market should consider trimming some of this exposure to reposition in other areas. Again, a balanced approach will be key.

Within U.S. equities, what other sectors or areas of the market could investors consider? From a market capitalization perspective, investors could go down

the capitalization range and consider small cap equities. Early last year, we identified the potential for small cap equities to outperform their large cap

brethren, a dynamic which we followed up in September with the piece titled “Small Cap Stocks: Waiting for Godot?” In this piece we stated that “Small cap stocks have persistently underperformed large caps for over a decade, but recent trends show signs of a potential turnaround, with small caps beginning to outperform in the short term as valuation gaps narrow and macro conditions shift…. Pro-growth policies such as tax cuts and deregulation, coupled with expectations of lower interest rates, and a historically wide valuation discount are potential catalysts for sustained small cap outperformance in the coming years.”

Since this piece was published last September, the performance gap between large- and small cap equities has become meaningfully narrower, to the point that we are starting to see small cap equity indices such as the Russell 2000 outperform the S&P 500, especially towards the end of last year and beginning of 2026. We believe that if pro-growth policies such as the Trump administration’s One Big Beautiful Bill, coupled with downward trending interest rates, materialize, the relative outperformance of small cap stocks could continue.

Pro-growth policies and lower interest rates should also affect U.S. equity markets at the sector level. As we said before, technology-oriented sectors have

been the undisputed market leaders over the past three years. However, other sectors such as Healthcare, Industrials, Financials, Utilities, and even certain industries within Energy, Materials, and Consumer Discretionary should also benefit if earnings growth expands into the rest of the economy and market breadth widens. The Healthcare and Industrials sectors should benefit, as both sectors are currently trading towards the lower half of their historical valuations, while also having the potential of benefiting from sector-specific themes. Healthcare could benefit from potentially lower regulation and an increased focus on longevity, while artificial intelligence increases productivity and efficiency in this sector over time. Industries such as biotech and medical technology should be beneficiaries of these themes. Along the same lines, the Industrials sector should see increased demand for robotics and automation, while increased geopolitical risk could propel the defense industry higher. At the same time, many companies in this sector should also benefit from increased spending on the

infrastructure needed for artificial intelligence and its increasing electrification needs.

The Financials sector could also see a move higher, as market volatility continues to drive trading revenues higher for large institutions, while smaller, regional banks could see increased loan demand if interest rates decrease. Lower interest rates also tend to benefit sectors with higher-yielding stocks, as investors tend to seek higher income, a dynamic that should benefit the Utilities sector. Additionally, some companies in this sector should also continue to benefit from the insatiable demand for power needed by the servers that enable artificial intelligence.

The Energy sector should also be a beneficiary of the AI boom. On one hand, sector valuations are at multiyear lows, while investors’ exposure to the sector remains at multi-decade lows. On the other hand, increased demand for power should increase production demand, especially from natural gas exploration and production companies. Similarly, a growing AI industry should cause many commodities within the Materials complex to continue to see increased demand, especially copper, nickel, and tin producers, along with silver and gold miners, albeit for different reasons. Steel producers could also see increased profit margins if interest rates trend lower, as construction demand should increase while costs of capital decrease. Although commodities tend to be volatile in nature, we continue to favor long term exposure to copper, silver, and gold.

Within the Consumer Discretionary sector, select industries such as e-commerce and discounted retailers should fare well this year, as lower rates, coupled with potential economic uncertainty, could increase demand for their products and services. It is important to note that a favorable disposition towards these sectors does not mean that we dislike the technology and communications sectors. On the contrary, we continue to find these sectors attractive over the long term, as we believe that strength will continue as the use and impact of artificial intelligence continues to grow. As such, investors should not eliminate exposure to these two sectors, as they continue to constitute an important piece of a diversified portfolio. Instead, investors should simply diversify their exposure to other sectors of the economy as well.

Our current year-end projection for the S&P 500 is 7,600, which is approximately 10% higher from its current level, close to 6,900, as of the time of this writing. This number is based on an earnings growth estimate between 12%-13%, predicated on the widening earnings base and sector rotation expounded upon above. However, as we know, along with opportunities also come risks. A crucial part of a sound investment strategy is to examine what could be missing, stress testing and attempting to find the weaknesses within our own narratives. In the world of investing, conviction can lead to great successes, blind love to great failures. I have always believed that we should treat a stock opposite the way we would treat a spouse or partner; never fall in love with or “marry” a stock, because the moment you do, you lose all rational objectivity.

With this in mind, some of the risks to our views on U.S. equities for 2026 could stem from various factors. Geopolitical risk is an ever-present factor to consider, particularly given the currently heightened geopolitical environment around the globe. A weaker than expected job market is another risk that we keep a very close eye on, as a sound employment base underpins continued economic growth. Higher than expected inflation is another factor that could quickly suffocate economic growth, a dynamic that could be unleashed by many factors, including higher commodity costs. A shallower than expected path in the reduction of interest rates also poses significant potential risks, as much of Wall Street’s base case for U.S. markets is based on a fairly predictable path for interest rates going forward. Lastly, increased political and regulatory risk at home could also create headwinds this year. Let us not forget that the U.S. will have mid-term elections in November, a dynamic that could quickly sway the political climate one way or another.

Given the many variables that inject risks into the markets, pullbacks are bound to happen during the year. On average, over the past 50 years, a 10-15% pullback has happened about once a year. It is part of the nature of equity markets. In fact, as we explored in the piece titled “Speculation at Hyperscale: Between AI Bubbles and Capex” some pullbacks are actually beneficial, as they take some of the proverbial froth off the markets and refresh investor perspectives. When pullbacks do happen,the important thing is to not lose sight of the longterm picture. Evaluating the opportunities and risks ahead of time is crucial in preparing our investmentportfolios for any type of environment.