May 29, 2026

SpaceX is preparing for what could be the largest IPO in history, targeting a valuation of USD 1.5–2.0 trillion, with proceeds of roughly USD 75–80 billion intended to fund the next phase of expansion across Starlink, Starship, AI infrastructure, and long-term orbital compute initiatives.

Despite its multiplanetary ambitions, SpaceX’s 2025 revenues of USD 18.7 billion remain largely driven by connectivity (Starlink) and launch services, with the AI segment still generating significant operating losses due to aggressive investment in large-scale data center infrastructure.

The IPO raises difficult questions around valuation, as investors are being asked to price not only current business lines but also highly speculative future markets such as orbital AI compute, space tourism, and asteroid mining — and at a valuation approaching USD 2 trillion, there will be very little room for execution mistakes.

Back in 1989, the space movie franchise Star Trek popu-larized the concept of the “final frontier,” a term that basi-cally refers to humanity exploring the last great unknown: outer space. While reading the offering memorandum for SpaceX’s initial public offering (IPO), it felt closer to reading a science fiction novel with attached financial statements than a traditional IPO filing. The more than 300-page document presenting Elon Musk’s largest and most ambitious project goes far beyond what we normally see in a corporate presentation and makes us wonder if we are potentially facing a great unknown for investors. The purpose of this piece is to provide a deeper analysis of what could become the largest IPO in history “from this planet.”

First, what exactly is SpaceX? SpaceX is an aerospace and technology company founded in 2002 by Elon Musk. The company develops reusable rockets, spacecraft, satellite communications infrastructure, and AI systems, with a long-term objective of reducing the cost of access to space and building large scale infrastructure in orbit.

Today, the company operates around three main pillars: space, connectivity, and artificial intelligence. In the space segment, SpaceX became the leading commercial

launch provider through its Falcon rocket family and reusable booster technology, significantly lowering launch costs while increasing launch frequency. In connectivity, the company built the Starlink satellite network, which now provides broadband and mobile connectivity globally through thousands of low Earth orbit satellites. Finally, on the AI side, following the inte-gration of xAI, SpaceX expanded into large scale AI infrastructure with the Colossus I & II construction and model development with its frontier model Grok.

More importantly, however, the company’s strategy is not to operate these businesses independently, but rather to integrate them into a single infrastructure plat-form. SpaceX expects to begin deploying orbital AI compute satellites as early as 2028, combining its launch capabilities, satellite manufacturing, Starlink connecti-vity network, and AI infrastructure into one vertically integrated ecosystem. The concept is straightforward, although highly ambitious: use space-based compute powered by solar energy to support large scale AI workloads while distributing those services globally through the Starlink network. In simple terms, SpaceX’s long-term vision is to leverage its satellite infrastruc-ture and launch capabilities to scale humanity’s access to energy and compute power in support of advanced artificial intelligence systems. Ultimately, the company believes these technologies could support a future multiplanetary economy.

While this still sounds closer to science fiction than to a traditional corporate strategy, it is worth remembering that, before Tesla, electric vehicles were not part of the mainstream conversation either, whereas today they are everywhere. Right now, concepts such as orbital AI or solar powered compute infrastructure in space may sound strange, but we simply do not know whether this could eventually become the next major corporate fron-tier. The key question, therefore, is not whether the story sounds ambitious, but rather what to do from an inves-tor’s perspective.

SpaceX is expected to go public in June 2026 in what could become the largest IPO ever. The company is reportedly targeting a valuation of approximately USD

1.5 – 2.0 trillion, with expected proceeds of roughly USD

75 to 80 billion, implying that around 4–5% of the company could initially be sold to public investors. While the final share count and pricing have not yet been offi-cially confirmed, the structure is expected to maintain strong insider control, with Elon Musk retaining most of the voting power through a dual-class share structure. The IPO’s main objective is not simply liquidity, but funding the next phase of expansion across Starlink, Starship, AI infrastructure, satellite manufacturing, and long-term orbital compute initiatives.

When analyzing the financial results, despite the company’s multiplanetary narrative, the reality is that current revenue streams are still generated by busi-nesses operating here on Earth. Therefore, before discussing orbital AI or future lunar infrastructure, it is important to take a deeper look into the company’s financial performance during 2025 and 1Q26. Spoiler, this looks like a Telecom company as of today.

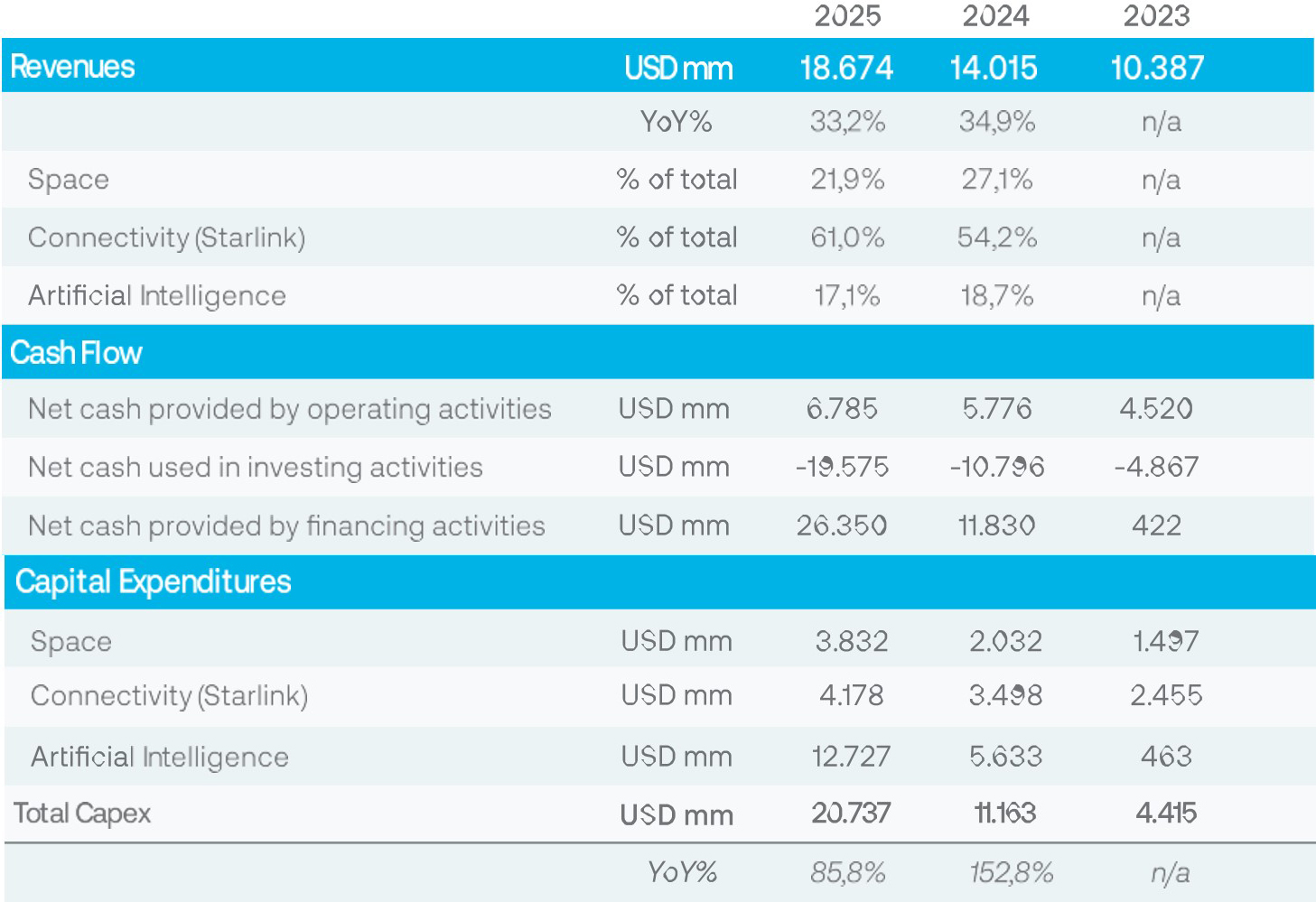

SpaceX revenues reached a staggering total of USD 18.7 billion in 2025, growing 33.2% year-over-year, represen-ting an increase of almost USD 4.7 billion compared to 2024. In addition, during 1Q26 alone, the company reported revenues of USD 4.7 billion, up 15% compared to the same period in 2025. While SpaceX has managed to generate positive operating cash flow during the last three years, its aggressive investment cycle, particu-larly related to AI infrastructure and compute develop-ment, has forced the company to increasingly rely on external financing to support operations, as reflected in Table 1.

While AI is clearly where the company has been focu-sing most of its investment efforts, the current revenue mix still looks very different.

On the space side of the business, revenue generated comes primarily from launch services provided to commercial companies, governments, and space agen-cies. SpaceX launches satellites, cargo, astronauts, and national security payloads using its Falcon Heavy rockets. Its largest customers include NASA, the U.S. Department of Defense, and commercial satellite operators.

For 2025, the space division reported revenues of USD 4.1 billion, a 7.6% increase year-over-year. Growth was mainly driven by additional Cargo Resupply Services provided to NASA and higher revenue from U.S. defense related contracts. Operationally, SpaceX continues to dominate the global launch market, reaching a total of 2,213 metric tons deployed into orbit during 2025 across 170 launches. Nevertheless, due to the heavy research and develop-ment costs associated with the Starship program (rockets designed to be refueled in orbit) and next

generation reusable launch systems, the segment reported a positive USD 653 million EBITDA but ultimately generated a net loss of USD 657 million during 2025.

On the connectivity front, revenue is generated through Starlink subscribers. Starlink is the satellite internet network created by SpaceX that uses thousands of low Earth orbit satellites to provide high-speed, low-latency broadband services to consumers, enterprises, and governments across 164 countries.

Starlink has almost quadrupled its subscriber base between 2023 and 2025, reaching approximately 10.5 million subscribers by the end of March 2026. This drove connectivity revenues to USD 11.3 billion, representing a 50% year-over-year increase. While the subscriber base increased, the company reported a 11.2% decline in Average Revenue per User (ARPU), mainly because of international expansion and lower priced service plans. Despite lower average pricing, the connectivity segment remains by far the company’s most profitable business line, reporting USD 7.2 billion in EBITDA and a USD 4.4 billion net gain for the year.

Finally, on the AI side, revenue is currently generated through advertising on the X platform (formerly Twitter), subscriptions to X and Grok, and data licensing agree-ments. During 2025, revenues reached USD 3.2 billion, representing year-over-year growth of 22.2%, mainly driven by higher advertising spending and increased subscriptions across both X and Grok products.

However, despite the increase in users and platform activity, the AI segment reported an operating loss of USD 6.3 billion during 2025. This was largely explained by the company’s aggressive investment cycle, including USD 5.1 billion allocated to research and development related to infrastructure and cloud computing capabilities.

According to the prospectus, much of this investment is tied to the launch of Colossus I and Colossus II, which the company describes as the largest AI training data center clusters currently operating on Earth. Together, these facilities provide approximately 1.0 gigawatt of compute power. To put this into context, most large-scale AI data centers today typically operate within a range of 100–300 megawatts of compute capacity, meaning SpaceX’s infrastructure is several times larger than most existing facilities.

On the balance sheet side, as of March 31, 2026, SpaceX reported cash and equivalents of USD 15.9 billion, current debt of USD 1.5 billion, and long-term debt of USD 28.7 billion. Long-term debt mainly consists of a USD 20.0 billion syndicated bridge loan maturing in September 2027. According to the filing, these funds have been used both to refinance existing obligations and to support investments in the company’s AI infrastructure segment. As reflected in Table 1, this financing activity drove an approximately USD 14 billion increase in cash flow from financing activities. Interest expense for 2025 stood at USD 1.8 billion.

Perhaps fixed income investors may not view SpaceX particularly favorably given its leverage profile and aggressive capital expenditure plans. However, for equity investors, this prospectus may represent exactly the type of asymmetrical opportunity many volatility-to-lerant investors may seek. One phrase in particular caught our attention: “we accept only the laws of physics as the limiting factors to our work and mission.”

In many ways, that single sentence summarizes the broader equity story being presented in this IPO.

Equity markets are constantly searching for companies capable of generating exponential returns, and this offe-ring memorandum clearly leans into that narrative. Throughout the document, the company references potential future markets including asteroid mining, space tourism, Mars cargo transport, off-world energy produc-tion, and manufacturing capabilities on the Moon and Mars. As mentioned previously, before Tesla, electric vehi-cles were barely part of the conversation. Therefore, even if some of these markets currently sound closer to science fiction than to traditional equity research models, they cannot simply be dismissed outright. That said, when looking at the current financial statements, SpaceX still resembles a telecommunications company far more than a fully integrated space-AI platform. This is not an early-stage startup; it is a company that has been opera-ting since 2002. Nevertheless, as reflected throughout the financial analysis above, the company is increasingly directing capital allocation toward AI infrastructure.

Why such an aggressive push into AI? The answer appears to be scarcity. Future AI growth may not be cons-trained by software itself, but rather by physical infrastruc-ture: compute power, energy availability, semiconductor supply, connectivity, and data center capacity. In that sense, SpaceX is effectively making a large-scale bet on vertically integrating both software and infrastructure scarcity into one ecosystem. More importantly, however, the company’s AI strategy does not stop on Earth. Concepts such as “orbital AI” involve moving compute infrastructure into space using satellites equipped with high-performance processors, solar power generation, and laser-based networking systems. The thesis is that space could eventually bypass some of Earth’s physical constraints related to energy, cooling, land availability, and power infrastructure.

From a valuation perspective, this creates an enormous challenge. Traditionally, investors would value each busi-ness segment independently and then aggregate them to estimate the total enterprise value. However, in such a unique and highly speculative environment, how should investors value the future economic potential of satellites powering AI infrastructure? Or more importantly, how should anyone discount the future cash flows of a hypo-thetical multiplanetary economy? At a valuation approa-ching USD 2 trillion, there will be very little room for execution mistakes, meaning SpaceX will ultimately become one of the largest execution stories public markets have ever seen. And markets have already shown that even exceptional execution may not always be enough. NVIDIA reported earnings on May 20, 2026, beating revenue expectations by more than 3%, yet the market reaction remained muted and the stock traded lower at the time of this report.

So why pursue the IPO now, particularly when expecta-tions around AI are already extremely elevated? While it is impossible to know the exact answer, one possible explanation is that the current AI boom has opened a unique financing window for technology companies. In fact, next week we will publish a separate piece discus-sing the broader IPO boom currently taking place across AI-related names. Earlier this year, on April 14, footwear company Allbirds announced plans to sell its footwear business to focus on AI infrastructure, causing the stock to surge more than 500% in a single day before even-tually retracing those gains.

Ultimately, the SpaceX IPO may represent one of the purest examples of markets financing a long-duration technological vision rather than current earnings power. Investors are not only buying launch services, broadband subscribers, or AI infrastructure; they are buying the possibility that SpaceX becomes a foundational layer of the future global economy. This is basically a bet on returns over capex. Whether that future materializes remains highly uncertain, but what is clear is that public markets are about to test how much value they are willing to assign to a company attempting to industrialize space, connectivity, and artificial intelligence simultaneously.

Important Disclosures

Insigneo Financial Group, LLC comprises a number of operating businesses engaged in the offering of brokerage and advisory products and services in various jurisdictions. Brokerage products and services are offered through Insigneo Securities, LLC, a broker-dealer registered with the U.S. Securities and Exchange Commission (“SEC”) and member of FINRA and SIPC. Investment advisory products and services are offered through Insigneo Advisory Services, LLC, an investment adviser registered with the SEC. Insigneo has affiliated companies in different locations, so it is important to understand which entity you are conducting business with. Please visit https://insigneo.com/legalentities/ for more information about the differences between these companies, their locations, and what that means for you.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security. It is for general information purposes only. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security. It does not constitute a recommendation or a statement of opinion, or a report of either of those things and does not, and is not intended, to consider the particular investment objectives, financial conditions, or needs of individual investors. Any target prices provide reflect our current expectations, are subject to change and may not be achieved due to a variety of risks, including changes in economic conditions, interest rates, geopolitical developments, and issuer-specific factors. The target price does not guarantee future results and should not be relied upon as a sole basis for investment decisions.

Not All Risks Are Disclosed – Past performance is not indicative of futures results. Investments involve significant risks, and it is possible to lose some or all of your principal investments and therefore may not be suitable for everyone. Always consider whether any investment is suitable for your particular circumstances and, if necessary, seek professional advice from your Investment Professional. This material may contain opinions, expressions, and estimates that represent the analysis and perspective of Insigneo Securities, LLC’s Investment Strategy department or its providers at the time of publication. These are subject to change at any time, without notice.

FOR AFFILIATES LOCATED IN CHILE

Insigneo Asesorías Financieras SPA se encuentra inscrito en Chile, en el Registro de Prestadores de Servicios Financieros de la Comisión para el Mercado Financiero. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de emisión de este. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera.

Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Asesorías Financieras SPA ni ninguna de sus empresas relacionadas.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta o solicitud de compra o venta de ningún valor en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en cuentas de corretaje y de asesoramiento de inversiones están sujetas al riesgo de mercado, incluida la pérdida de capital.

La información base del presente informe puede sufrir cambios, no teniendo Insigneo Securities LLC ni Insigneo Asesorías Financieras SPA la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la

ocurrencia de tales cambios. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.

FOR AFFILIATES LOCATED IN URUGUAY

Insigneo Asesor Uruguay S.A. está inscripto en el Registro de Mercado de Valores del Banco Central del Uruguay como Asesor de Inversiones. En Uruguay, los valores están siendo ofrecidos en forma privada de acuerdo al artículo 2 de la ley 18.627 y sus modificaciones. Los valores no han sido ni serán registrados ante el Banco Central del Uruguay para oferta pública. Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted según su perfil y estrategia de inversión. Este documento no constituye un asesoramiento ni una recomendación u oferta o solicitud de compra o. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso. Rentabilidades históricas de los productos anunciados no aseguran rentabilidades futuras..

FOR AFFILIATES LOCATED IN ARGENTINA

Insigneo Argentina S.A.U. Agente Asesor Global de Inversión se encuentra registrado bajo el N° 1053 de la Comisión Nacional de Valores (CNV) e inscripto ante la Inspección General de Justicia (IGJ) bajo el N° 12.278 del Libro 90, Tomo –, de Sociedades por Acciones. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de su emisión. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera. Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Argentina S.A.U. ni ninguna de sus empresas relacionadas. La información base del presente informe puede sufrir cambios, no teniendo Insigneo Argentina S.A.U. la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta, recomendación o solicitud de compra o venta de ningún valor negociable en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.