May 19, 2026

The April IMF publications are seeing the current global shock as structural rather than cyclical, with geopolitical tensions amplifying fiscal stress, shrinking policy space, and creating asymmetric outcomes across countries rather than broad-based relief.

Rising public debt and persistently higher interest rates are narrowing governments’ room to maneuver just as inflation, defense spending, and weaker growth further erode fiscal buffers, in-creasing sensitivity to policy credibility.

Latin America enters this period with a mixed but relatively stronger starting point, benefiting selectively from higher energy prices and stronger institutions, even as inflation risks, slowing growth, and political uncertainty complicate the outlook.

espite macro headwinds, regional fixed income has shown resilience and continues to offer selective opportunities that favor fundamental theses rather than broad exposure.

The global economy in 2026 finds itself navigating a far more complex and fragile landscape than many anticipated at the start of the year. What began as a gradual post-pandemic normalization and recovery from the price dislocations associated with Libera-tion Day, has been disrupted by the escalation of conflict in the Middle East. While much of the im-mediate focus has centered on energy markets and commodity price dynamics, a more consequential and underappreciated dimension of this shock lies in its implications for the global fiscal outlook.

Recent publications from the International Monetary Fund, including the April 2026 Fiscal Monitor and Regional Economic Outlook for the Western Hemi-sphere, provide a useful framework for understanding how this geopolitical development is reshaping fiscal trajectories across both advanced and emerging economies. The Fund’s assessment is clear: the current environment is not merely cyclical in nature but reflects a structural deterioration in fiscal conditions, compounded by tighter financial constraints and elevated geopolitical uncertainty.

At the global level, the IMF characterizes the fiscal impact of the Middle East conflict as highly asymmetric. Low-income, energy-importing economies are expected to bear the brunt of the adjustment, facing higher import costs, weaker growth, and limited policy flexibility. In contrast, the group of beneficiaries is narrower than in previous commodity shocks, as even traditional energy exporters – particularly in the Gulf – are directly exposed to the conflict’s broader economic and financial spillovers. This asymmetry under-scores a key point: the current shock is less conducive to broad-based fiscal relief and more likely to exacerbate divergence across countries.

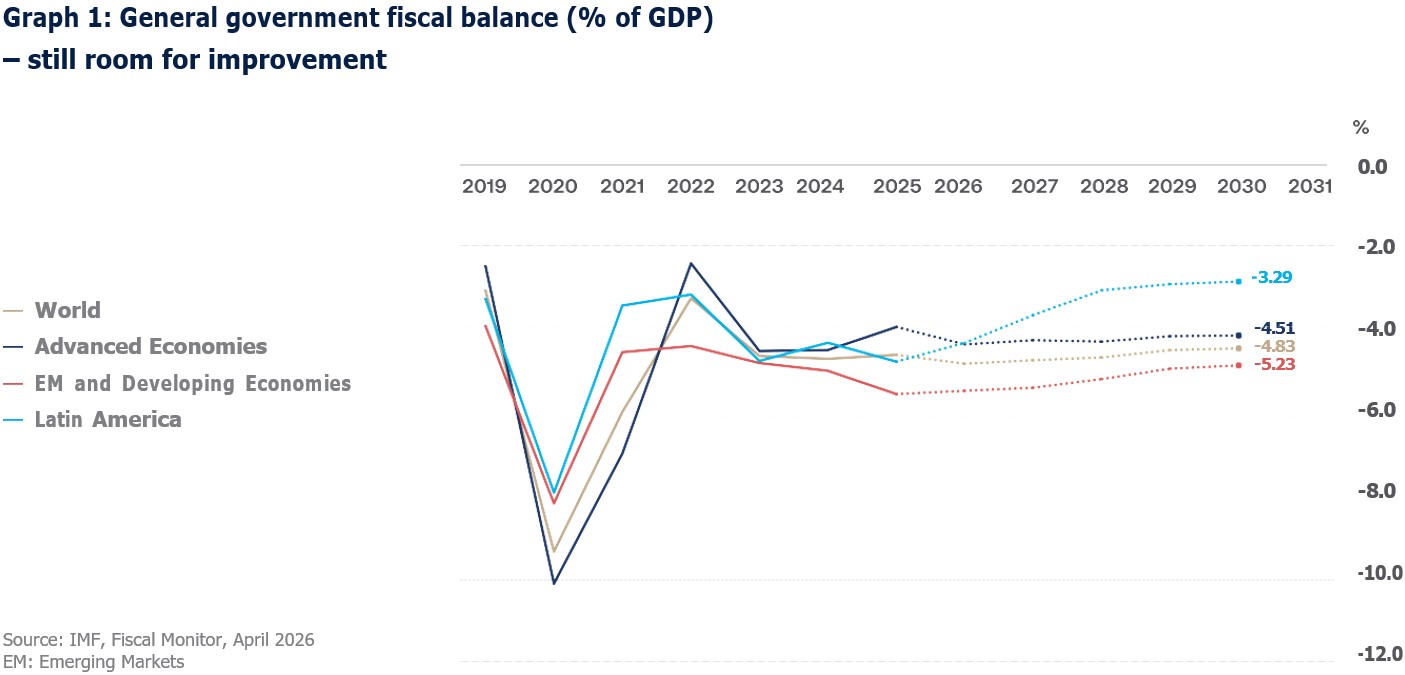

Perhaps more concerning is the trajectory of global public debt. The IMF now projects that global gross debt will approach 100% of GDP by 2029, a level not seen since the aftermath of World War II. This projection is especially troubling when considered alongside today’s higher interest rate environment and increased market sensitivity to fiscal slippage. Governments are therefore operating with a much narrower margin for error, as the cost of borrowing remains elevated and investor tolerance for fiscal deterioration has diminished. In practical terms, the space for countercyclical fiscal policy is shrinking at precisely the moment when it may be most needed.

The conflict itself is expected to reinforce these pressures through multiple transmission channels.

Higher food and energy prices will continue to feed into inflation, while tighter financial conditions and slower economic activity weigh on revenue generation. At the same time, rising defense expenditures are likely to place additional strain on already stretched government budgets. The cumulative effect is a further erosion of fiscal buffers across much of the global economy.

Against this challenging backdrop, the IMF emphasizes the importance of institutional strength as a key differentiator. Emerging markets that have in-vested in credible macroeconomic frameworks – such as independent central banks, inflation-targeting regimes, and robust local currency debt markets – are better positioned to absorb external shocks. This observation is particularly relevant when assessing the outlook for Latin America, a region that enters this period with a mixed but, in relative terms, somewhat more favorable starting point (see graph 1).

From a macroeconomic perspective, Latin America stands to benefit modestly from higher energy prices, particularly in oil-exporting economies such as Brazil, Colombia, and Guyana. Improved terms of trade in these countries are expected to support external balances, provide a degree of fiscal relief, and underpin economic activity. Indeed, the IMF suggests that, on net, several of these economies may experience a positive economic impact from the current environment. However, these gains are neither uniform nor sufficient to offset the broader challenges facing the region.

Inflation remains a central concern across Latin America, regardless of a country’s energy profile. Rising fuel and transportation costs, alongside higher food prices and input costs, are feeding into broader price pressures. Recent data already point to a reacceleration of inflation in several key economies. Peru, for instance, has experienced a notable uptick driven by fuel price shocks, disruptions in natural gas supply, and adverse climate conditions. Mexico and Colombia have also seen increases in both headline and core inflation, with Colombia facing an additional layer of uncertainty related to concerns over central bank independence.

In response to these dynamics, central banks across the region have adopted a cautious and data-dependent stance. The uncertainty surrounding the duration and potential escalation of the Middle East conflict has reduced visibility on the inflation path, prompting policymakers to favor a more measured approach to interest rate decisions. Rather than rush-ing into easing cycles, most institutions are signaling a willingness to wait for clearer evidence before ad-justing policy, thereby preserving credibility while try-ing to anchor inflation expectations.

At the same time, growth dynamics are beginning to show signs of moderation. Recent activity indicators suggest that economic momentum is softening in several major economies, including Mexico, Brazil, and Chile, where year-over-year growth readings have turned negative. Colombia continues to expand but at a decelerating pace, while Peru stands out as a relative bright spot, with activity levels remaining close to potential. This emerging divergence within the re-gion highlights the importance of country-level differ-entiation when assessing investment opportunities.

Fiscal conditions, while comparatively more stable than in other regions, remain a source of vulnerability. Brazil and Colombia, in particular, exhibit some of the largest fiscal deficits and highest debt burdens in Lat-in America. These challenges are further complicated by upcoming electoral cycles, which introduce the risk of policy shifts toward increased public spending. In both countries, the political landscape suggests the possibility of administrations that may favor ex-panded subsidy programs and looser fiscal discipline. Absent credible spending controls, such developments could exacerbate existing fiscal imbalances and undermine investor confidence.

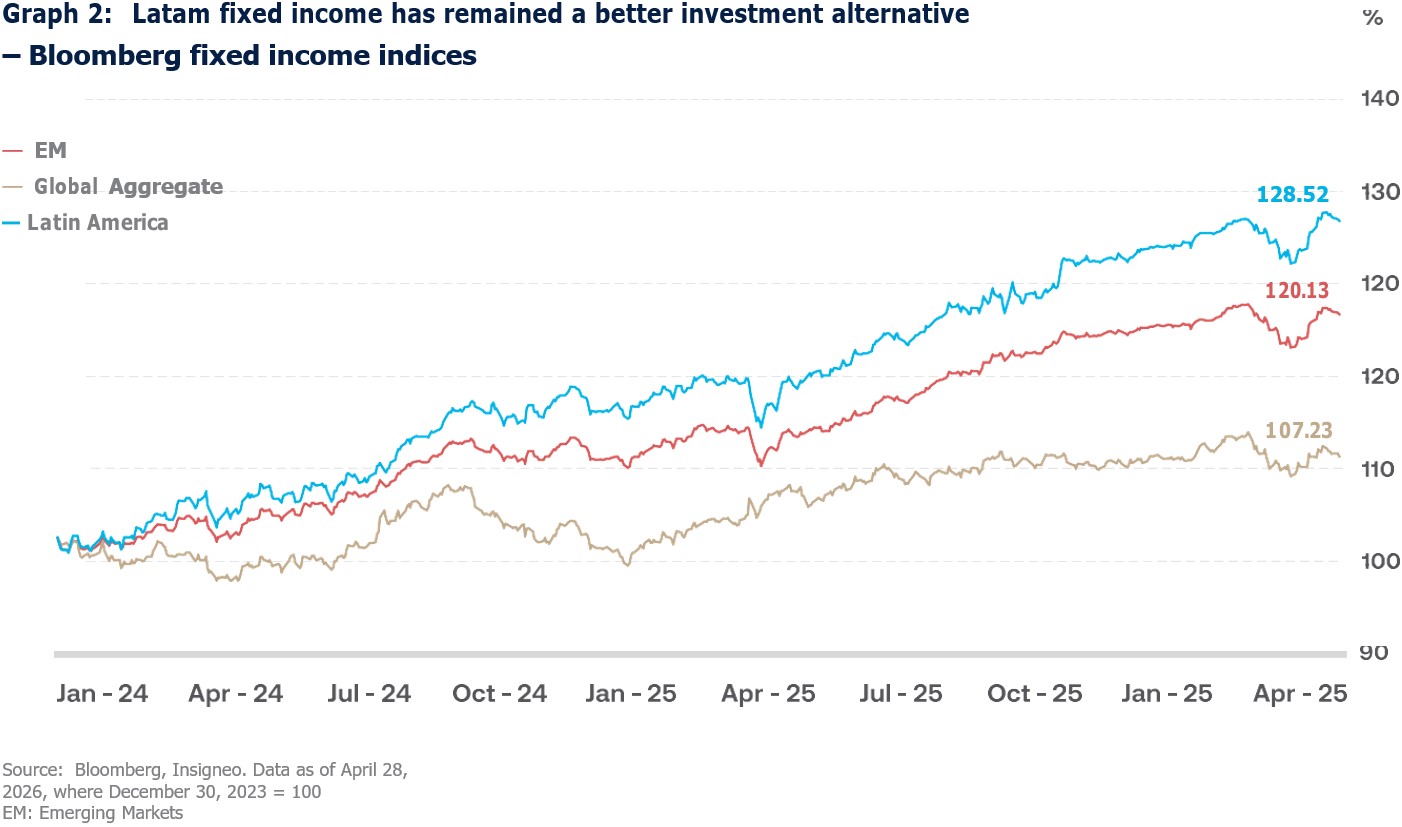

Despite these macroeconomic and fiscal headwinds, Latin American fixed income has demonstrated no-table resilience. Over the past two years, the region has outperformed both the broader emerging mar-ket complex and global aggregate bond indices, re-flecting a combination of attractive carry, improving institutional credibility, and relatively disciplined monetary policy (see graph 2). This performance un-derscores the region’s continued relevance within global portfolios, particularly in an environment where yield remains scarce and differentiation across emerg-ing markets is increasingly pronounced.

From an investment standpoint, the current environ-ment reinforces the importance of selectivity and the-matic positioning. Broad-based exposure to the re-gion is unlikely to deliver optimal outcomes; instead, investors should focus on specific “pockets of value”

where macro tailwinds and structural drivers align. One such area is the North American integration theme, where a potential extension of the T-MEC agreement would benefit companies leveraged to nearshoring and regional supply chain realignment, including issuers such as Cemex, Banorte, and Fibra Uno. Another area of interest lies in Argentina’s ener-gy sector, where continued development of the Vaca Muerta formation and associated infrastructure proj-ects could unlock significant value. Companies such as YPF, Vista Energy, and Pampa Energía are well po-sitioned to capitalize on this opportunity, provided that investment momentum is sustained.

Ultimately, the investment landscape in Latin America – and indeed globally – is being shaped by a conflu-ence of forces that include geopolitical fragmentation, fiscal constraints, and persistent inflationary pressures. In such an environment, the case for diversified and actively managed portfolios becomes particularly compelling. Investors must balance regional and sectoral exposures while maintaining a disciplined focus on issuer fundamentals and policy credibility.

In conclusion, while Latin America is not insulated from the challenges facing the global economy, it offers a combination of relative resilience and selective opportunity. Commodity-linked advantages and identifiable areas of structural growth provide a foundation for outperformance, albeit within a highly uncertain and evolving context. Navigating this landscape will re-quire not only a clear understanding of macroeconomic dynamics but also a rigorous, bottom-up approach to investment selection.

Insigneo Financial Group, LLC comprises a number of operating businesses engaged in the offering of brokerage and advisory products and services in various jurisdictions. Brokerage products and services are offered through Insigneo Securities, LLC, a broker-dealer registered with the U.S. Securities and Exchange Commission (“SEC”) and member of FINRA and SIPC. Investment advisory products and services are offered through Insigneo Advisory Services, LLC, an investment adviser registered with the SEC. Insigneo has affiliated companies in different locations, so it is important to understand which entity you are conducting business with. Please visit https://insigneo.com/legalentities/ for more information about the differences between these companies, their locations, and what that means for you.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security. It is for general information purposes only. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security. It does not constitute a recommendation or a statement of opinion, or a report of either of those things and does not, and is not intended, to consider the particular investment objectives, financial conditions, or needs of individual investors. Any target prices provide reflect our current expectations, are subject to change and may not be achieved due to a variety of risks, including changes in economic conditions, interest rates, geopolitical developments, and issuer-specific factors. The target price does not guarantee future results and should not be relied upon as a sole basis for investment decisions.

Not All Risks Are Disclosed – Past performance is not indicative of futures results. Investments involve significant risks, and it is possible to lose some or all of your principal investments and therefore may not be suitable for everyone. Always consider whether any investment is suitable for your particular circumstances and, if necessary, seek professional advice from your Investment Professional.

This material may contain opinions, expressions, and estimates that represent the analysis and perspective of Insigneo Securities, LLC’s Investment Strategy department or its providers at the time of publication. These are subject to change at any time, without notice.

FOR AFFILIATES LOCATED IN CHILE

Insigneo Asesorías Financieras SPA se encuentra inscrito en Chile, en el Registro de Prestadores de Servicios Financieros de la Comisión para el Mercado Financiero. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de emisión de este. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera.

Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Asesorías Financieras SPA ni ninguna de sus empresas relacionadas.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta o solicitud de compra o venta de ningún valor en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en cuentas de corretaje y de asesoramiento de inversiones están sujetas al riesgo de mercado, incluida la pérdida de capital.

La información base del presente informe puede sufrir cambios, no teniendo Insigneo Securities LLC ni Insigneo Asesorías Financieras SPA la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.

FOR AFFILIATES LOCATED IN URUGUAY

Insigneo Asesor Uruguay S.A. está inscripto en el Registro de Mercado de Valores del Banco Central del Uruguay como Asesor de Inversiones. En Uruguay, los valores están siendo ofrecidos en forma privada de acuerdo al artículo 2 de la ley 18.627 y sus modificaciones. Los valores no han sido ni serán registrados ante el Banco Central del Uruguay para oferta pública. Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted según su perfil y estrategia de inversión. Este documento no constituye un asesoramiento ni una recomendación u oferta o solicitud de compra o. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso. Rentabilidades históricas de los productos anunciados no aseguran rentabilidades futuras.

FOR AFFILIATES LOCATED IN ARGENTINA

Insigneo Argentina S.A.U. Agente Asesor Global de Inversión se encuentra registrado bajo el N° 1053 de la Comisión Nacional de Valores (CNV) e inscripto ante la Inspección General de Justicia (IGJ) bajo el N° 12.278 del Libro 90, Tomo –, de Sociedades por Acciones. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de su emisión. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera. Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Argentina S.A.U. ni ninguna de sus empresas relacionadas. La información base del presente informe puede sufrir cambios, no teniendo Insigneo Argentina S.A.U. la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta, recomendación o solicitud de compra o venta de ningún valor negociable en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.