April 24, 2026

The “fog of peace” – a period of uncertainty, confusion, and miscommunication, despite the lack of active warfare- is becoming entrenched in the Middle East. While both the United States and Iran likely want some form of resolution, major disagreements make stable peace unclear, raising the risk of a prolonged “frozen conflict.”

For investors, despite geopolitical uncertainty, markets are shifting their focus back to funda- mentals, with potential long-term impacts of the conflict including a higher floor on oil prices, as well as higher demand for energy, commodities, and defense spending, reinforcing the importance of diversification and disciplined, long-term positioning.

Many of us have heard about the “fog of war”. Often occurring during the heat of battle, it is a period fraught with miscommunication, confusion, and uncertainty. In other words, a time of utter informa- tional chaos, when no one is exactly sure what is going on or what is going to happen next. As the antithesis to war, however, peace tends to be a moment exemplified by better clarity, communica- tion, and a higher degree of certainty. But what about a period that is filled with miscommunication, confu- sion, and uncertainty, but where warring countries are not engaged in active warfare, and are arguably seeking some form of resolution? Could this be considered the “fog of peace”? We think so.

This appears to be the current state of the conflict with Iran. What is clear is that, after nearly two months of war, a protracted conflict is not in the best interest of anyone involved. As a result, even if the United States, Israel, and Iran may not be preparing for long lasting peace, they are looking for some form of resolution, which has currently taken shape as a fragile cease-fire. However, no one really knows how the conflict will end. It is easy to see how, if a cessa- tion of hostilities with no substantial agreement is achieved, this tenuous truce could morph into a “frozen war” which could remain in place for the fore- seeable future. However, “frozen wars” tend to thaw quickly and flare up violently, especially in geopoliti- cally hot places like the Middle East. A misstep by either side, particularly Iran, could quickly lead to the renewal of active conflict. In the absence of a substantive peace agreement, it appears likely that tensions in the region will continue, in some form or another, for the foreseeable future.

The current state of the conflict begs the following question: How can investors position their portfolios to successfully navigate the situation at hand? First, we want to avoid taking risks based on what we think we can see through the fog but have no realistic foundation on which to base our decision. As a result, investors should avoid trying to invest based on the slew of everchanging headlines. Second, we want to evaluate some of the possible long-term implications of the conflict and analyze potential opportunities. However, it is crucial to keep in mind that in a scenario involving a high degree of uncertainty, such as the current “fog of peace”, balance and objectivity are key.

Much like a ship currently sailing into the Strait of Hormuz, markets appear unclear as to what lies ahead in the uncharted waters of this conflict. Interestingly though, despite the potential unknowns on the horizon, it appears as if investors are starting to look past many of these risks. Case in point is the relationship between oil and U.S. equity markets. At the onset of the conflict and through its first month, Brent Oil prices and the S&P 500 had a strong nega- tive correlation; as oil jumped higher, equity markets retreated. This negative correlation remained in place even after the cease-fire was first announced on April 7th, although this time, as oil pulled back, markets moved higher. However, over the past week or so, we have begun to see the correlation between both markets turn positive, with both moving in the same direction. The reason for this change could be a combination of two factors. First, in the absence of

active conflict, market participants appear to have become desensitized to the ever-changing head- lines pointing towards war or peace. At the same time, earnings season has begun to play out in the

U.S. Lacking any meaningful headlines in the evolu- tion of the conflict, investors appear to have shifted their attention towards company earnings, to gauge the potential effects of the war.

To this point, the potential investment implications from the conflict on equity markets abound, but some are more salient than others. Below we explore some of the sectors, industries, and regions that could be impacted by the conflict.

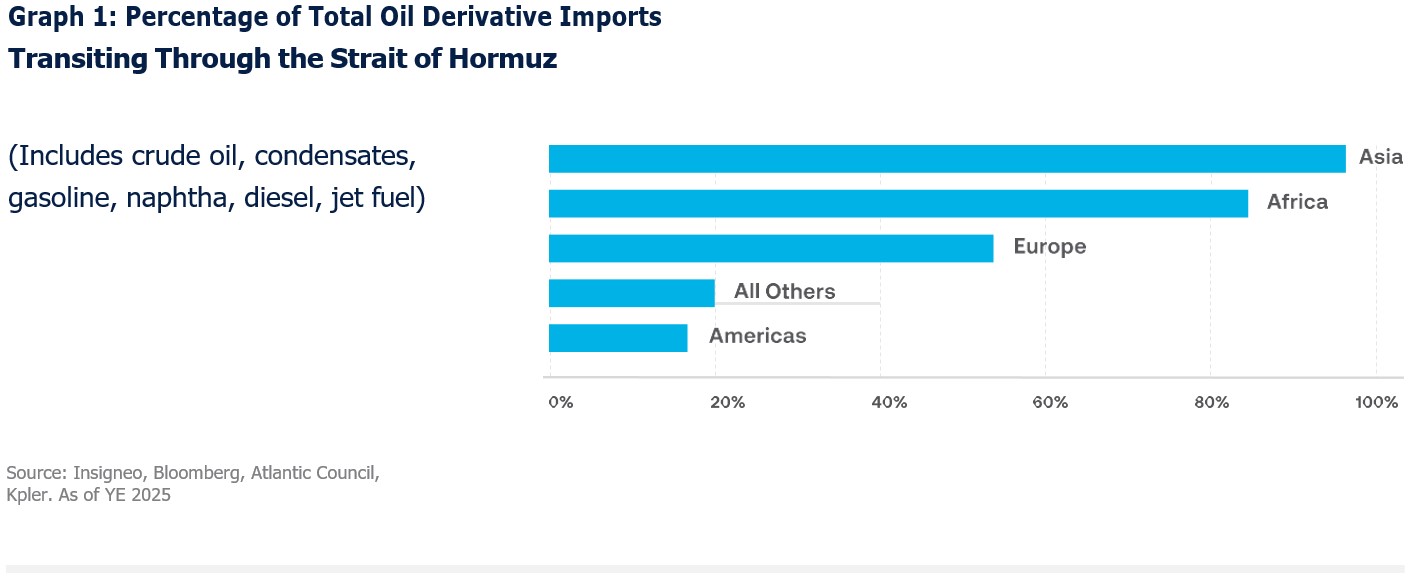

The current conflict has highlighted the painful dependence of many regions around the world on Middle Eastern supplies of oil and gas. The graph below shows the percentage of each region’s total oil derivative imports that stem from the Middle East that must transit through the Strait of Hormuz. As we can see from the graph, the region most affected by the closure of the Strait is Asia, as approximately 90% of its oil needs to flow through this waterway. Africa is in second place, and Europe comes in third, seeing more than half of its oil supplies in peril. Despite this meaningful number, the oil and gas situ- ation in Europe could potentially be understated, as the region depends heavily on the Middle East for its imports of jet fuel. Such is Europe’s reliance on this region, that the International Energy Agency estimates that if the Strait continues to remain closed, flight cancellations in Europe could begin within weeks.

In fact, some airlines such as Lufthansa and KLM have already started to reduce their routes. Interestingly though, as we can see on the graph, the Americas is the region least affected by disruptions

in the Strait, as many countries in this region, such as the Unites States, Canada, Brazil, and Colombia, are net exporters of oil and gas.

An important point that the conflict has brought to light is the fact that individual countries need to focus on stockpiling strategic commodities, including oil; something that China has been doing for years. In fact, the U.S. Energy Information Administration estimates that China holds a reserve of approximately 1.4 billion barrels of oil, making it the largest national stockpile of oil in the world, with approximately two years’ worth of reserves. The supply shortfalls exposed by the conflict will likely cause other countries to follow suit, stockpiling not only oil, but other critical commodities such as gas, copper, lithium, rare earths, and gold, among others. As a result, oil and gas producers in the Energy sector such Chevron, Diamondback Energy, EQT, Petrobras, YPF, and Vista Energy could benefit over the long term, as increased demand will likely lead to increased production. At the same time, increased geopolitical risk will likely lead to a higher floor for oil prices, potentially improving margins for many of these companies. In the Materials sector, copper miners such as Freeport-McMoran, Southern Copper, and Vale, lithium miners such as Sociedad Quimica y Minera de Chile, and gold miners such as Barrick Mining and PanAmerican Silver could also potentially benefit from increased commodity prices.

Current commodity supply chains are certainly more resilient than they were during the Covid-19 pandemic, supported by more distribution options as well as built-in redundancies. However, a full return to pre-war operations will take time. The Boston Consulting Group estimates that if the Strait of Hormuz were to reopen tomorrow, it would take approximately 18 to 24 months for supplies to return to normal across global industries. At the same time, countries are still likely to attempt to build up more robust supply cushions, increasing stockpiling behavior and potentially driving commodity prices higher. A final point to consider is that some of these oil and gas supply lines, such as pipelines and refin- eries, which were damaged during the war, will need to be repaired, potentially increasing demand from oil & gas services providers and engineering and construction companies such as SLB, Haliburton, and Baker Hughes.

In addition to commodities, another global industry that is likely to see increased demand because of the conflict is the defense industry. Both the United States and Israel will continue to invest heavily in the modernization of their weapons systems, as well as the replenishment of munition stockpiles expended during the conflict. At the same time, Europe is likely to continue to spend on modernizing its own armed forces, a dynamic that first began during the conflict between Russia and Ukraine. Increased spending on defense driven by heightened geopolitical risk could potentially benefit companies such as Boeing, Lockheed Martin, Northrop Grumman, L3 Harris, and RTX. Additionally, the current conflict with Iran has brought to light the reality that irregular warfare is an effective way to wage war for countries with restricted military budgets, such as Iran and Ukraine. There are many facets to irregular warfare, but one involves the use of low-cost, mass produced systems such as drones and relatively inexpensive ballistic missiles to effectively provide what is known as theater area denial. What this means is that low-cost systems can make it much harder for larger, conventional armies to operate freely in hostile territory. We are currently seeing this dynamic playout in the Strait of Hormuz. The conflict has shown that conventional forces will have to integrate irregular warfare systems into their own operations, which could potentially benefit the companies listed above, as well companies such as Palantir Technologies and privately held drone maker Anduril Industries.

At the regional level, we continue to believe that a balanced portfolio diversified across the United States, Europe, and Emerging Markets constitutes the best strategy to navigate the current uncer- tainty in the markets.

In our 2026 U.S. Equities Market Outlook published in January, before the war started, we stated: “Our year- end S&P 500 target of 7,600 is based on 12–13% earnings growth and sector rotation; however, inves- tors should remain balanced and vigilant given risks from various factors such as geopolitics, inflation, interest-rate paths, labor markets, and political uncertainty, and be prepared for normal market pull- backs…While large-cap tech should continue to grow, its dominance is likely to normalize, with small caps and sectors such as Industrials, Healthcare, Financials, Utilities, Energy, Materials, and select Consumer Discretionary areas contributing more meaningfully as market breadth widens.” The conflict in Iran has not changed our thesis for U.S. equity markets, and we continue to believe that a balanced approach, at both the sector and market level is the best approach to weathering the current situation.

Selectively positioning ourselves within Emerging Markets, we believe that Latin America could poten- tially be a net beneficiary of the conflict with Iran. In our 2026 International Equities Market Outlook also published in January, we stated: “One of our favorite regions with the Emerging Markets complex is Latin America. Driven in large part by increasing earnings growth potential, Latam equities experienced some of the strongest moves in 2025. However, we believe that there is further growth potential ahead for the region, as many of its commodity export-driven economies will continue to benefit from a weaker U.S. Dollar, while growth in specific industries such as fintech, could propel earnings growth higher. At the same time, as evidenced by the recent elections in Argentina and Chile, the region appears to be experi- encing a political shift to the right. This may mean that incoming governments could implement busi- ness-friendly policies that may increase regional investment and consumption, possibly driving earn- ings higher. This year’s upcoming elections in Brazil, Colombia, and Peru will be pivotal in the continuation of this trend and ones that we will be watching closely.” Although the conflict with Iran has pushed the USD higher, the increased demand for commod- ities engendered by the conflict has also led to increased demand for exports from the region. We believe that this dynamic is likely to continue, which should prove to be a tailwind for the fortunes of regional companies.

As of the time of this writing, a tenuous cease-fire in the Iran conflict remains in place. While each side raises allegations over ceasefire violations, both continue to enforce their own versions of a naval blockade of the Strait of Hormuz. The U.S. Central Command reports that the U.S. Navy has forced 31 Iranian-linked vessels to return to port, while the Wall Street Journal reports that Iran seized 3 vessels and fired upon others. Confusion over the control of the Strait of Hormuz, as well as miscommunication and uncertainty over negotiations between both parties, continue. The U.S. has stated that it is has extended the cease-fire and is waiting for Iran to put forth an updated proposal, while Iran says that it will not come to the negotiation table until the US blockade is lifted. The confusion, miscommunication, and uncertainty

associated with the “fog of war” continue to swirl in the proverbial gulf of demands that linger between the belligerents. The “fog of peace” still lays thick over the Middle East. In scenarios fraught with uncertainty, focusing on what we know, not on what we do not know is crucial. Remaining objective, keeping a balanced portfolio, and maintaining our focus on the long term are key.

As a matter of full disclosure, the Insigneo Latin American Equity Portfolio holds positions in some of the companies listed above. It is important to keep in mind that the individual equities referenced here can exhibit high degrees of volatility and are not suitable for every investor. These investments are best considered on a case-by-case basis, based on a particular investor’s willingness and ability to tolerate risk. If you need more information or would like to discuss these potential ideas in more detail, please do not hesitate to contact your financial advisor.

Insigneo Financial Group, LLC comprises a number of operating businesses engaged in the offering of brokerage and advisory products and services in various jurisdictions. Brokerage products and services are offered through Insigneo Securities, LLC, a broker-dealer registered with the U.S. Securities and Exchange Commission (“SEC”) and member of FINRA and SIPC. Investment advisory products and services are offered through Insigneo Advisory Services, LLC, an investment adviser registered with the SEC. Insigneo has affiliated companies in different locations, so it is important to understand which entity you are conducting business with. Please visit https://insigneo.com/legalentities/ for more information about the differences between these companies, their locations, and what that means for you.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security. It is for general information purposes only. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security. It does not constitute a recommendation or a statement of opinion, or a report of either of those things and does not, and is not intended, to consider the particular investment objectives, financial conditions, or needs of individual investors. Any target prices provide reflect our current expectations, are subject to change and may not be achieved due to a variety of risks, including changes in economic conditions, interest rates, geopolitical developments, and issuer-specific factors. The target price does not guarantee future results and should not be relied upon as a sole basis for investment decisions.

Not All Risks Are Disclosed – Past performance is not indicative of futures results. Investments involve significant risks, and it is possible to lose some or all of your principal investments and therefore may not be suitable for everyone. Always consider whether any investment is suitable for your particular circumstances and, if necessary, seek professional advice from your Investment Professional. This material may contain opinions, expressions, and estimates that represent the analysis and perspective of Insigneo Securities, LLC’s Investment Strategy department or its providers at the time of publication. These are subject to change at any time, without notice.

FOR AFFILIATES LOCATED IN CHILE

Insigneo Asesorías Financieras SPA se encuentra inscrito en Chile, en el Registro de Prestadores de Servicios Financieros de la Comisión para el Mercado Financiero. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de emisión de este. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera.

Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Asesorías Financieras SPA ni ninguna de sus empresas relacionadas.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta o solicitud de compra o venta de ningún valor en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en cuentas de corretaje y de asesoramiento de inversiones están sujetas al riesgo de mercado, incluida la pérdida de capital.

La información base del presente informe puede sufrir cambios, no teniendo Insigneo Securities LLC ni Insigneo Asesorías Financieras SPA la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.

FOR AFFILIATES LOCATED IN URUGUAY

Insigneo Asesor Uruguay S.A. está inscripto en el Registro de Mercado de Valores del Banco Central del Uruguay como Asesor de Inversiones. En Uruguay, los valores están siendo ofrecidos en forma privada de acuerdo al artículo 2 de la ley 18.627 y sus modificaciones. Los valores no han sido ni serán registrados ante el Banco Central del Uruguay para oferta pública. Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted según su perfil y estrategia de inversión. Este documento no constituye un asesoramiento ni una recomendación u oferta o solicitud de compra o. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso. Rentabilidades históricas de los productos anunciados no aseguran rentabilidades futuras..

FOR AFFILIATES LOCATED IN ARGENTINA

Insigneo Argentina S.A.U. Agente Asesor Global de Inversión se encuentra registrado bajo el N° 1053 de la Comisión Nacional de Valores (CNV) e inscripto ante la Inspección General de Justicia (IGJ) bajo el N° 12.278 del Libro 90, Tomo –, de Sociedades por Acciones. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de su emisión. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera. Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Argentina S.A.U. ni ninguna de sus empresas relacionadas. La información base del presente informe puede sufrir cambios, no teniendo Insigneo Argentina S.A.U. la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta, recomendación o solicitud de compra o venta de ningún valor negociable en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.