March 6, 2026

The high‑yield market has regained momentum as issuers show a renewed willingness to return to primary markets, supported by a more construc‑ tive macro backdrop and moderated recession concerns.

A noticeable migration of lower‑rated issuers to‑ ward leveraged loans is reshaping the HY universe and contributing to its higher overall credit quality.

Performance trends show high yield – especially BBs – continuing to outpace investment‑grade, underscoring the market’s preference for yield‑driven exposures.

Despite this constructive setup, pockets of stress, sector‑specific underperformance, and recent defaults underscore the need for disciplined cred‑ it selection in a volatile environment.

“You don’t find out who’s been swimming naked until the tide goes out.”

– Warren Buffet

Fixed income, particularly high yield corporate credit debt, has regained its footing after the 2022 draw‑ down, helped by the long‑anticipated easing cycle and a renewed wave of issuer refinancing activity. With volatility elevated in early 2026, we wanted to take a closer look at the U.S. high yield market to as‑ sess how issuers and investors are positioning, what current pricing and flows are signaling, and what this implies for credit conditions over the coming months.

First, let us refresh the definition of high yield. High yield debt, sometimes referred to as junk bonds, is debt issued by companies whose credit rating is be‑ low ‘BBB‑’. These issues tend to offer a higher yield to compensate for the lower credit quality of the issuer, which could also involve higher risks for investors.

The renewed appetite for high yield debt has been underpinned by the observed interest from issuers in returning to the market. According to data compiled by Bloomberg Intelligence, 2022 was the year with the smallest total high yield debt issued since 2013; meanwhile, the period between 2023 and 2025 saw a recovery in high yield debt issuance. To put things into perspective, total gross high yield issuance in 2022 stood at ~USD 118bn, which contrasts with the ~USD 368bn issued in 2025. The return of issuers to the debt market is occurring against a more benign macroeconomic backdrop of relatively resilient economic growth and recession concerns kept at bay. Still, some inflation and employment fears are looming in the U.S. economy, mainly stemming from a stickier than expected PCE inflation and a labor market that continues to face downside risks.

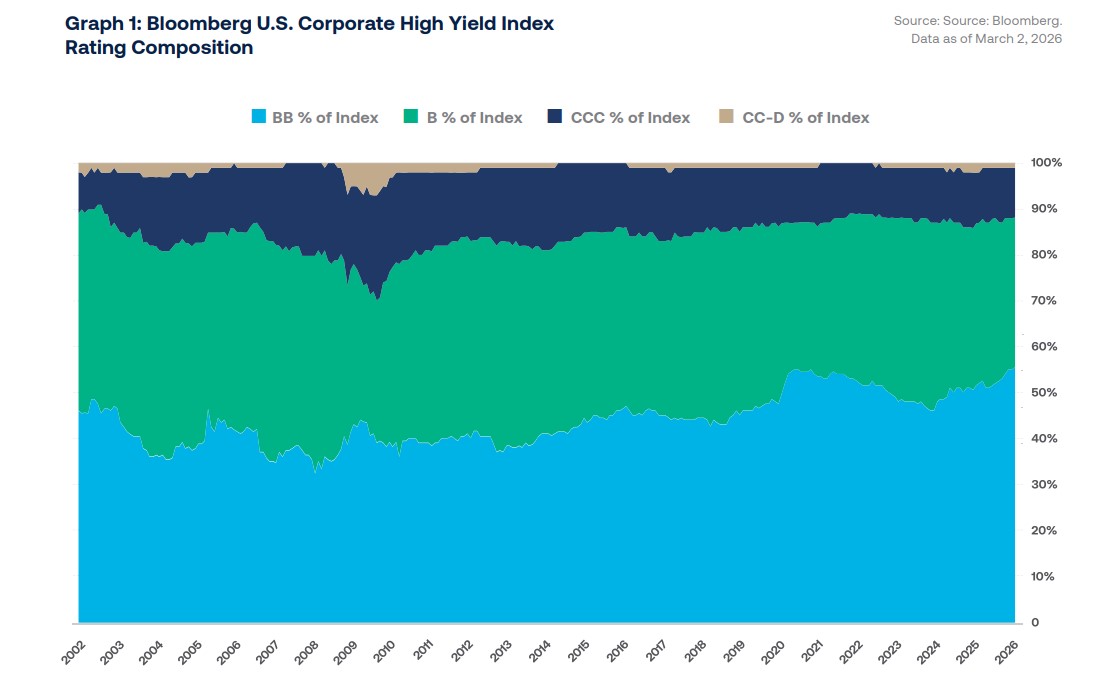

Now, let us zoom in on the high yield segment, repre‑ sented by the Bloomberg US Corporate High Yield Total Return Index. Within the index, the share of BB bonds in the index has increased steadily since the early 2000s and currently makes up 56% (see graph 1). It is also worth noting that, even if it has decreased since the early 2000s, the share of B bonds has re‑ mained relatively steady and currently sits at 33%. Comparatively, lower‑quality securities have main‑ tained a smaller representation within the index, with CCC bonds being 11% and CC‑D securities being the remaining 1%.

Another point worth highlighting is the reduction in the participation of lower‑rated names within the debt in‑ dex. This is a phenomenon that may be partially ex‑ plained by the observed migration from the high yield market into leveraged loans. It is important to note that this migration does not remove any previously existing credit risk, it only transfers it to a different segment. To this point, according to data compiled by Bloomberg Intelligence, as of February 2026, issuance of leveraged loans stood at ~USD 41.7bn, whereas most of that issu‑ ance was either refinancing or repricing of loans. It is also worth stressing that most loans issued in February, according to S&P’s rating scale, were either ‘B‑’ or ‘B’ rated. This shift within the high yield debt market has led to, almost inherently, an improvement in issuer quality.

In terms of performance, after the pandemic, and even more so after 2022, high-yield debt has been an overperformer, beating IG on a consistent basis. For 2025, the HY debt universe was the sole outper‑ former, being closely followed by the BB index. Mean‑ while, IG debt and, more specifically, BBB bonds, ex‑ hibited less stellar performance (see graph 2). It is worth noting that high yield debt is an alternative for investors who have a higher risk tolerance and who, ultimately, are looking to implement what is known as a carry trade – an investment strategy in which returns come primarily from collecting the yield (the “carry”) on a bond, rather than from betting on changes in interest rates or credit spreads.

It is also worth mentioning that carry trades tend to work best during periods of spread stability, which was the case for most of 2025 when, aside from the volatility peak caused by the Liberation Day an‑ nouncements, the Bloomberg U.S. HY index exhibit‑ ed an Option Adjusted Spread – OAS – that averaged ~296bps.

Even if the performance of HY debt has been very positive, we would be remiss if we did not stress some factors that could emerge as potential cracks for the public credit markets.

One of the first points we need to stress is that even if the OAS spread from the HY index is still close to its multi-year low, the recent geopolitical events are starting to cause spreads to widen. Taking into ac‑ count that there is a considerable amount of uncer‑ tainty surrounding the duration of the current conflict, it would not be surprising to see a continuation of this widening trend.

Against this backdrop, and even if it sounds counter- intuitive in a sector of the market that is sometimes referred to as “junk”, it is more important than ever to assess quality before investing. This is more import‑ ant if we consider that, aside from rising geopolitical volatility, the high yield market recently experienced two defaults (Tricolor Holdings and First Brands) at the end of 2025 that already eroded investors’ sentiment.

Additionally, the high yield index for the technology sector, together with the high yield index for finance companies, are the two subsectors with the worst year‑to‑date performance. This is taking place amid a surge of data center building in the U.S. needed to finance the AI boom that is also being financed by high yield issuers. In addition, private credit concerns have recently rattled the public debt markets through headlines surrounding Blue Owl and the UK’s mort‑ gage provider Market Financial Solution (MFS). What stands out even more is the increased participation of debt financing in deals that were typically in the realm of equity financing, but due to the size of said projects, companies need all financing alternatives on deck.

“Even if the OAS spread from the HY index is still close to its multi-year low, the recent geopolitical events are starting to cause spreads to widen. ”

As we move forward in this rapidly changing environ- ment, where volatility and unexpected events are shaping the way investors position their portfolios, quality becomes the name of the game. We strongly believe that debt from an issuer with solid funda- mentals will always be the best alternative for any fixed income portfolio. Through careful, thorough credit selection, one can ensure that investors are compensated and shielded during peak volatile peri‑ ods. Issuers with a strong capacity to generate oper‑ ating income and operating cash flows will also be available in the high yield market, with those charac‑ teristics serving as their differentiating factor from other issuers. To quote Warren Buffet, “you don’t find out who’s been swimming naked until the tide goes out”, and investors should not want debt in their port‑ folios that could be caught swimming naked in funda‑ mental terms.

Insigneo Financial Group, LLC comprises a number of operating businesses engaged in the offering of brokerage and advisory products and services in various jurisdictions. Brokerage products and services are offered through Insigneo Securities, LLC, a broker‑dealer registered with the U.S. Securities and Exchange Commission (“SEC”) and member of FINRA and SIPC. Investment advisory products and services are offered through Insigneo Advisory Services, LLC, an investment adviser registered with the SEC. Insigneo has affiliated companies in different locations, so it is important to understand which entity you are conducting business with. Please visit https://insigneo.com/legalentities/ for more information about the differences between these companies, their locations, and what that means for you.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security. It is for general information purposes only. To the extent that this material discusses general market activity, industry or sector trends or other broad‑based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security. It does not constitute a recommendation or a statement of opinion, or a report of either of those things and does not, and is not intended, to consider the particular investment objectives, financial conditions, or needs of individual investors. Any target prices provide reflect our current expectations, are subject to change and may not be achieved due to a variety of risks, including changes in economic conditions, interest rates, geopolitical developments, and issuer‑specific factors. The target price does not guarantee future results and should not be relied upon as a sole basis for investment decisions.

Not All Risks Are Disclosed – Past performance is not indicative of futures results. Investments involve significant risks, and it is possible to lose some or all of your principal investments and therefore may not be suitable for everyone. Always consider whether any investment is suitable for your particular circumstances and, if necessary, seek professional advice from your Investment Professional.

This material may contain opinions, expressions, and estimates that represent the analysis and perspective of Insigneo Securities, LLC’s Investment Strategy department or its providers at the time of publication. These are subject to change at any time, without notice.

Insigneo Asesorías Financieras SPA se encuentra inscrito en Chile, en el Registro de Prestadores de Servicios Financieros de la Comisión para el Mercado Financiero. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de emisión de este. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera.

Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Asesorías Financieras SPA ni ninguna de sus empresas relacionadas.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta o solicitud de compra o venta de ningún valor en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en cuentas de corretaje y de asesoramiento de inversiones están sujetas al riesgo de mercado, incluida la pérdida de capital.

La información base del presente informe puede sufrir cambios, no teniendo Insigneo Securities LLC ni Insigneo Asesorías Financieras SPA la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.

Insigneo Asesor Uruguay S.A. está inscripto en el Registro de Mercado de Valores del Banco Central del Uruguay como Asesor de Inversiones. En Uruguay, los valores están siendo ofrecidos en forma privada de acuerdo al artículo 2 de la ley 18.627 y sus modificaciones. Los valores no han sido ni serán registrados ante el Banco Central del Uruguay para oferta pública. Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted según su perfil y estrategia de inversión. Este documento no constituye un asesoramiento ni una recomendación u oferta o solicitud de compra o. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso. Rentabilidades históricas de los productos anunciados no aseguran rentabilidades futuras.

Insigneo Argentina S.A.U. Agente Asesor Global de Inversión se encuentra registrado bajo el N° 1053 de la Comisión Nacional de Valores (CNV) e inscripto ante la Inspección General de Justicia (IGJ) bajo el N° 12.278 del Libro 90, Tomo –, de Sociedades por Acciones. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de su emisión. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera. Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Argentina S.A.U. ni ninguna de sus empresas relacionadas. La información base del presente informe puede sufrir cambios, no teniendo Insigneo Argentina S.A.U. la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta, recomendación o solicitud de compra o venta de ningún valor negociable en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.