March 27, 2026

Insigneo’s Quarterly Call Q2 2026:

“Second-Order Opportunities”

As I write, the war involving Iran has entered a more precarious and consequential phase. For the first time in this conflict, oil and gas produc- tion facilities across the region have been deliberately targeted by both Israel and Iran. In efFect, the war appears to be approaching an inflection point: either both sides step back and avoid further attacks on economi- cally critical assets, or the conflict escalates into a more punitive phase with the potential to inflict lasting damage on energy infrastructure of global significance. Setting aside the moral and humanitarian dimensions of the war, the only thing that matters for investors right now, the market’s central concern, is that commodities continue to flow through Hormuz.

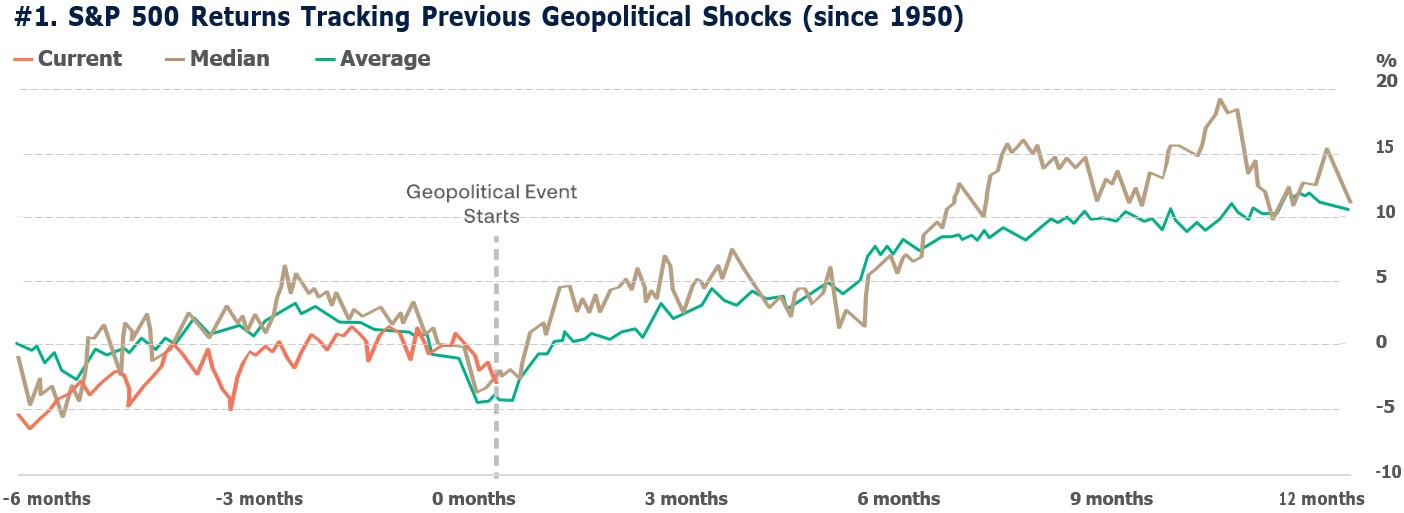

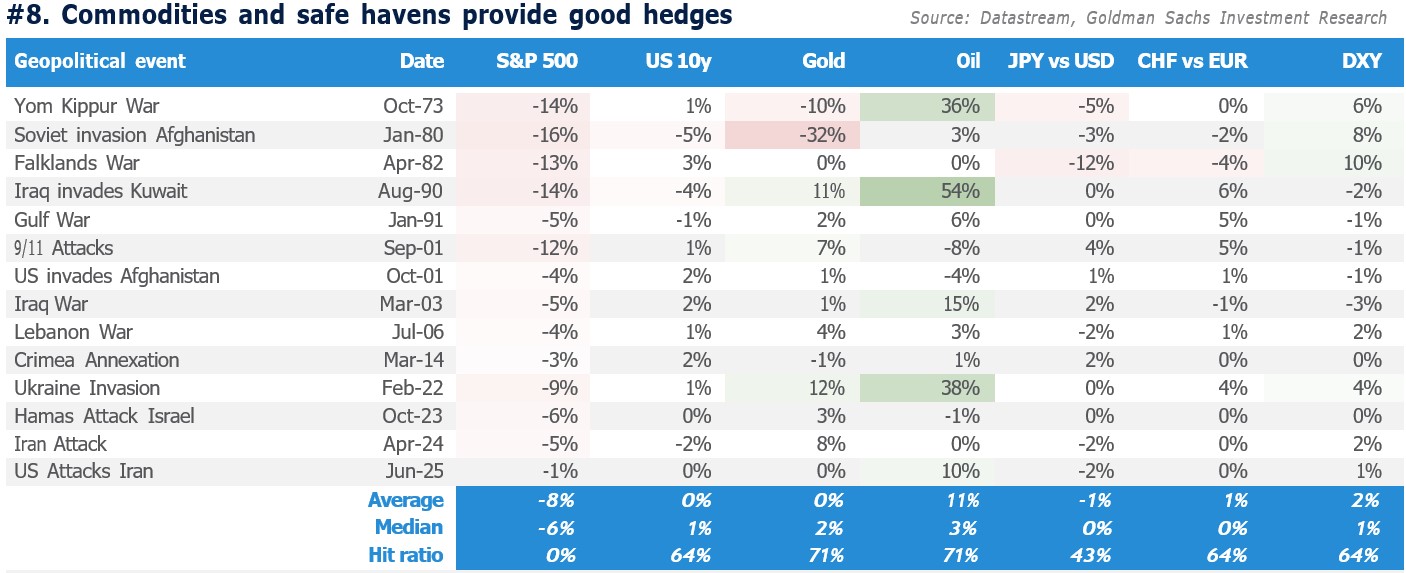

Our base case is that they will, and soon enough to avert a global reces- sion – and particularly a U.S. recession. In our view, both sides retain meaningful incentives to de-escalate: Iran’s closest partners need the Strait to resume normal shipping, while the Trump Administration and Congressional Republicans remain constrained by domestic political considerations, especially control of the U.S. Senate. If that view proves correct, the current market dislocation is likely to look, twelve months from now, like little more than a brief and barely perceptible interruption. The broader macroeconomic backdrop remains constructive, supported by resilient global fundamentals and AI-driven productivity gains that continue to lift corporate earnings. History also ofFers some perspective: since 1950, the median S&P 500 return one year after a geopolitical shock has been more than 11% as shown in Chart 1. Indeed, the Russia-Ukraine war triggered similar fears in 2022 around energy, food, and broader commodity supply. Yet while that conflict remains ongoing and devas- tating, markets eventually moved on once they recalibrated to the reality that critical commodity flows would continue.

That is precisely why the present moment matters so much. Some, and quite possibly most, of the disrupted volume is likely to resume flowing, and there are already tentative signs pointing in that direction. Beyond its own tankers, Iran has continued to allow Chinese, Indian, and Iraqi vessels to transit the Strait, and the United States has so far tolerated that arrange- ment. There are even indications that Iran is imposing fees on ships for passage through Hormuz. Earlier this year, when the probability of military strikes began to rise, we advised Insigneo Advisors to hedge portFolios

through a tactical long oil position, despite our more bearish longer-term view on crude prices. One week into the conflict, as Brent approached

$100 per barrel, we recommended closing only halF of that hedge. The remaining position is still in place today, and we expect to remove it once we have greater confidence that our base-case de-escalation scenario is unfolding as anticipated.

Although a recession does not appear imminent, the probability has clearly increased. As of today, our subįective U.S. recession model assigns a 35% probability to a downturn this year, up from 20% last month. In other words, while recession is not our base case, we see a materially higher risk that the situation could deteriorate. Risk assets have already begun to reflect some of that downside, though markets still appear far from pricing in a true worst-case scenario – namely, a prolonged disrup- tion that culminates in a global recession. In this quarterly letter, we revisit our macroeconomic outlook, assess what has changed and what has not, and outline the portFolio adįustments we believe are most relevant for investors in the coming quarter and over the balance of the year. Our central focus, however, is on the second- and third-order efFects of this conflict: the consequences that remain underappreciated, including both the known unknowns and the unknown unknowns. Those risks are real. History repeatedly reminds us that it only obeys one law – the law of unin- tended consequences. These are often the most consequential, and investors must remain alert to them, both to manage risk efFectively and to identify the opportunities they may create.

The Iran war has reached a critical inflection point: the key market issue is not the conflict itself, but whether energy and commodity flows through the Strait of Hormuz remain largely intact.

Our base case remains one of de-escalation. Both Iran and its trading partners, as well as U.S. political actors, have strong incentives to avoid a prolonged disruption that would materially damage global growth.

Recession risk has risen meaningfully, but reces- sion is still not our base case. Our models suggest a wider distribution of outcomes, with “contained damage” still the most likely macro scenario.

The main transmission channel is oil: higher energy prices tighten financial conditions, lift near-term inflation, weaken real income growth, and reduce central banks’ room to ease policy quickly.

Even so, the broader macro backdrop remains more resilient than headlines imply. U.S. growth, corporate earnings, business investment, and AI-driven productivity trends continue to provide a meaningful cushion.

For markets, short-term correction risk is real, but longer-term prospects remain constructive so long as the conflict does not lead to a lasting loss of productive capacity in the Middle East.

Portfolio strategy should therefore be two-speed: more defensive and quality-focused in the near term, while remaining selectively pro-risk over a 12-month horizon.

We favor resilience now, including quality equities, cash, gold, and TIPS, while maintaining conviction in medium-term themes such as AI, infrastructure, energy security, defense, and other real-asset- linked opportunities.

Earnings remain the key reason not to become overly bearish. Valuation expansion may be harder from here, but profit growth still provides support for equities over time.

The conflict is also accelerating deeper structural shifts: a more multipolar world, greater focus on strategic resources and supply chains, and a broader rotation toward real assets, security-linked sectors, and regional integration themes, including selective opportunities in Latin America.

Bottom line: respect the short-term risks, but do not capitulate to them. If Hormuz disruptions fade rather than intensify, periods of weakness are more likely to prove tactical opportunities than the start of a lasting bear market.

The macro picture has unquestionably become more complicated, but it is not yet broken. Our view is that recession risk has risen meaningfully as the

Iran shock has worsened the near-term growth-in- flation tradeoff; even so, the global economy still appears resilient enough to absorb the shock, provided the disruption is not prolonged and does not lead to a sustained loss of productive capacity in the Middle East. In our Annual 2026 Outlook

published in January, we projected U.S. real GDP growth of 2.0% for 2026, and for now that forecast remains unchanged. Prior to the outbreak of this conflict, stronger-than-expected first-quarter data and solid corporate earnings led us to consider revising that estimate up to 2.2%. We are holding off on any such adjustment until there is greater clarity on how the conflict evolves and concludes.

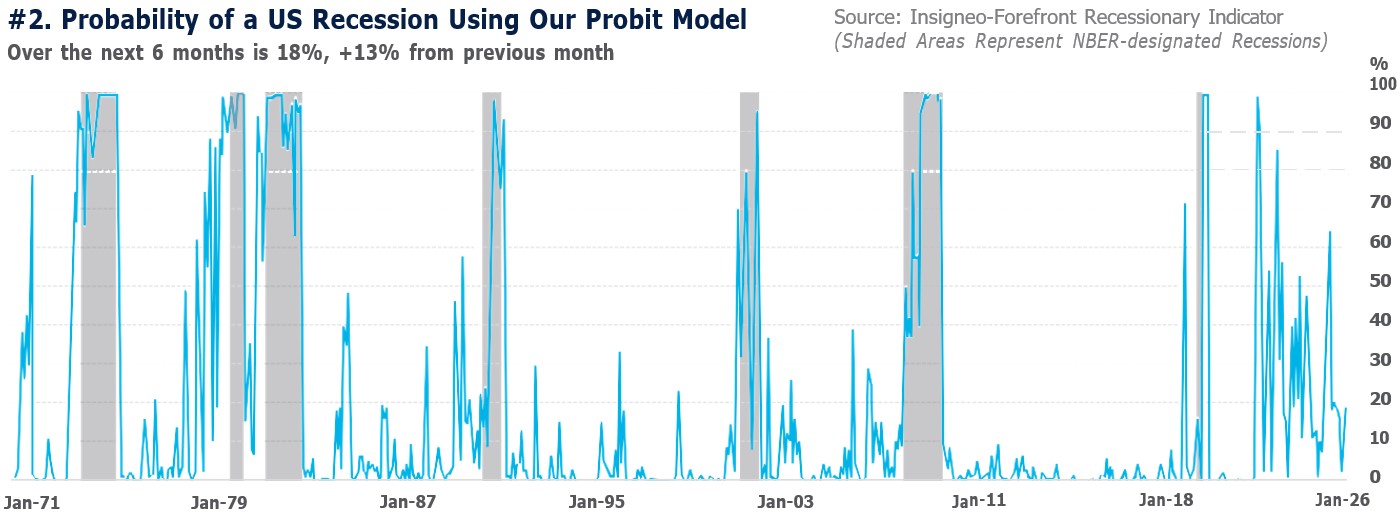

Our quantitative Insigneo-Forefront Recessionary Indicator currently implies an 18% probability of a U.S. recession over the next six months, as shown in Chart 2. As noted earlier, our subjective framework assigns a 35%

probability of a contraction. Taken together, the message is not that a recession is imminent, but rather that the distribution of risks has widened materially. The Iran conflict has introduced a classic oil-shock transmission mechanism into an expansion that had otherwise remained reasonably intact: higher energy prices, tighter financial conditions, more cautious central banks, and weaker real-income growth. Even so, an outright global contraction is not our base case, largely because the futures curve still points to at least partial normalization in energy prices over time and because the U.S. economy is materially less oil-intensive than in it was in prior decades.

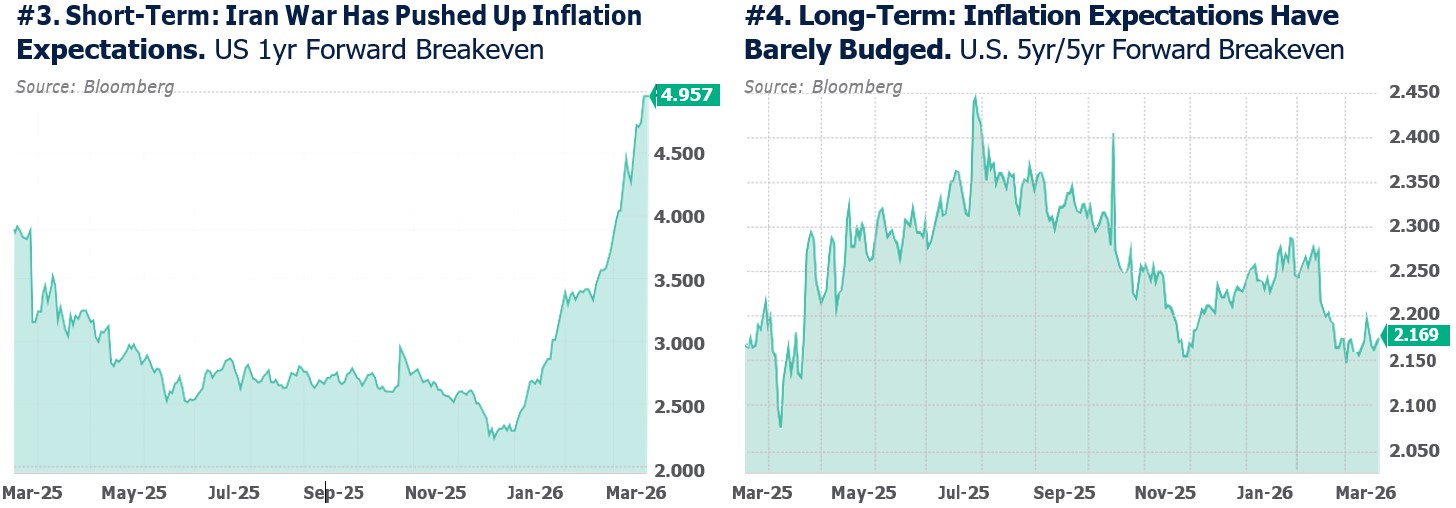

Chart 3 and Chart 4 together frame the inflation debate well. In the short run, the shock is plainly inflationary. The U.S. 1-year breakeven has almost doubled since early January, and 1-year CPI swaps have risen 130bps in the Eurozone. But the longer end has remained much more contained, consis- tent with a market view that this is a relative-price shock rather than the start of a new secular inflation regime. In other words, near-term inflation has wors- ened, but long-term inflation credibility has not yet been lost. That distinction is critical because, in our view, it explains why policy easing has been delayed rather than canceled outright. We now expect rate cuts not to materialize until the back half of the year.

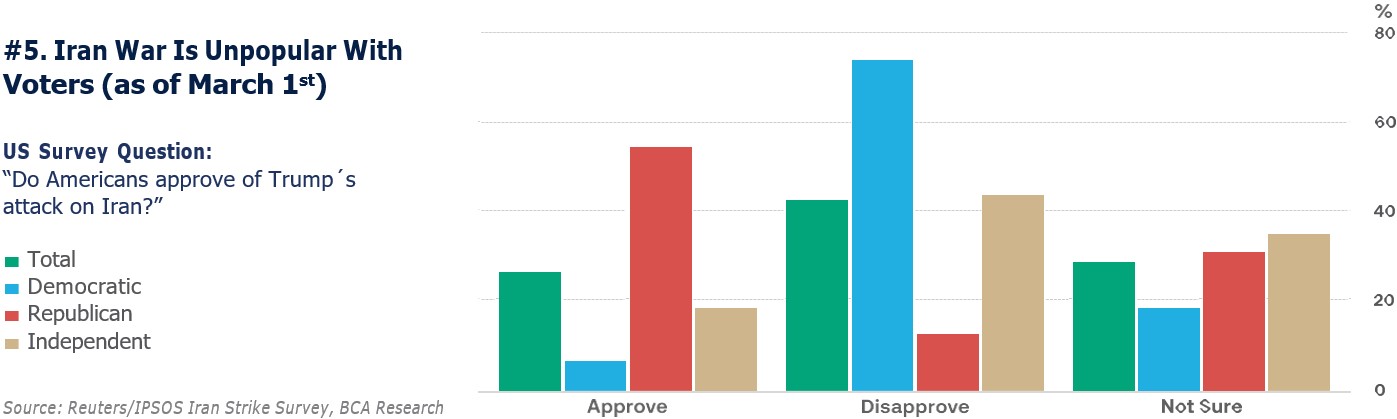

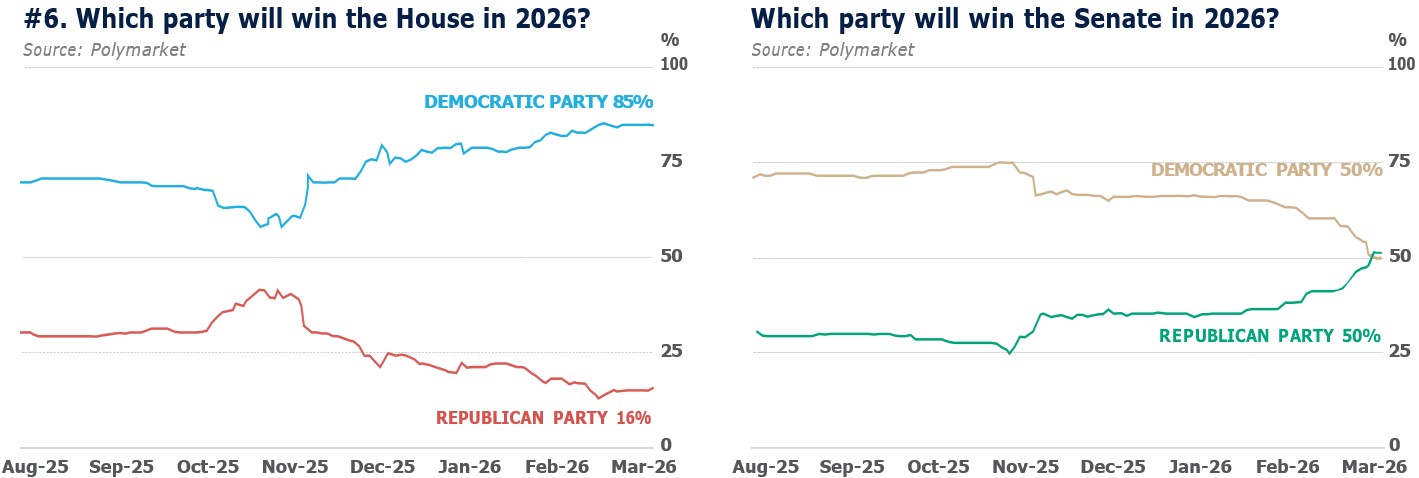

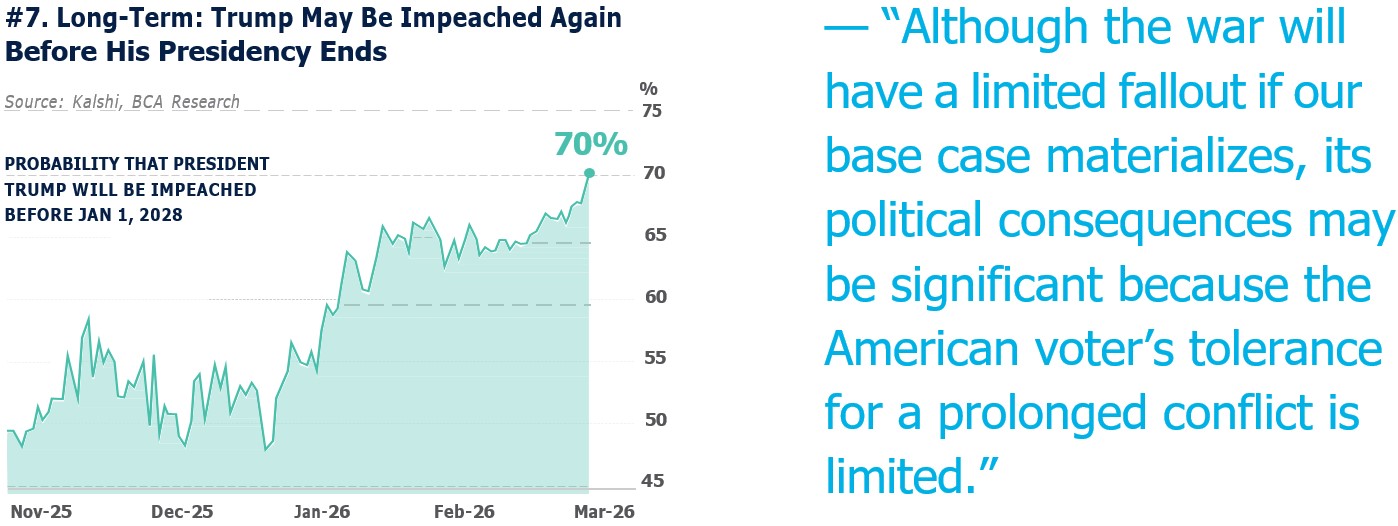

Although the war will have a limited fallout if our base case materializes, its political consequences may be significant because the American voter’s tolerance for a prolonged conflict is limited (see Chart 5, Chart 6, Chart 7). This is why we argued that both Iran and the U.S. have incentives to find an off-ramp, even if the path is messy and nonlinear. For markets, that matters because the single most important macro variable is not simply the level of oil prices, but the duration of the disruption. A short, violent shock is manageable. A prolonged interruption to flows, shipping, or productive capacity is the scenario that would more seriously threaten global growth.

Our bottom line on the macro-outlook, therefore, is straightforward. Growth is slowing at the margin, inflation has become firmer in the near term, and

the Fed has less flexibility to ease policy as quickly as markets had anticipated at the start of the year. Even so, the cycle itself remains intact. Labor markets are softer than they were in 2022, which leaves the economy somewhat more vulnerable, but earnings, business investment, and productivity trends have not meaningfully rolled over. Our base case is not one of “no damage,” but rather one of “contained damage.” The principal risk is that oil prices remain elevated for long enough to undermine demand, prompt broader earnings downgrades, and ulti- mately trigger a more serious recession scare.

The market outlook follows directly from our macro framework: correction risk remains real in the short term, but the medium- to longer-term back- drop is more constructive than the headlines would suggest. Chart 8 points to the clearest immediate portfolio implications. In the near term, portfolios should be built to be more resilient. In practice, that means adopting a more defensive posture, emphasizing higher-quality exposures, and being more selective about where inflation and

geopolitical hedges are deployed. Accordingly, we favor becoming tactically more defensive over the next three months while remaining modestly pro-risk over a twelve-month horizon, with a prefer- ence for quality equities, cash, gold, and TIPS as portfolio ballast against stagflationary spillovers.

The most important reason not to become overly bearish here is that earnings have held up materially better than price action – and that distinction matters.

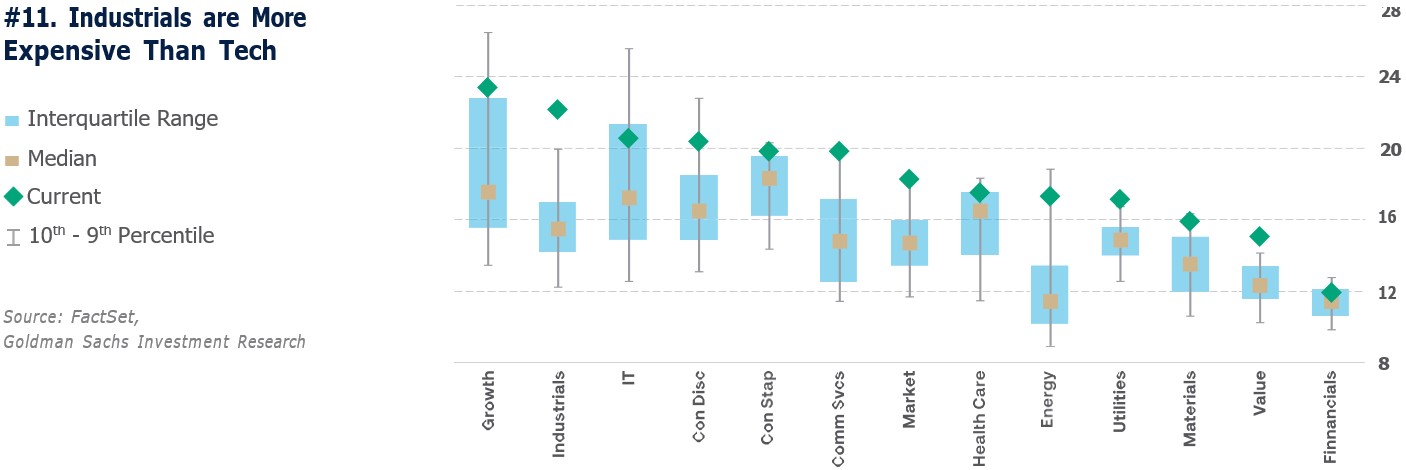

— “With valuations across regions and sectors high, cyclicals trading in line with defensives, and global Industrials becoming more expensive than IT, it means that the old cyclical catch-up trade has lost some appeal.”

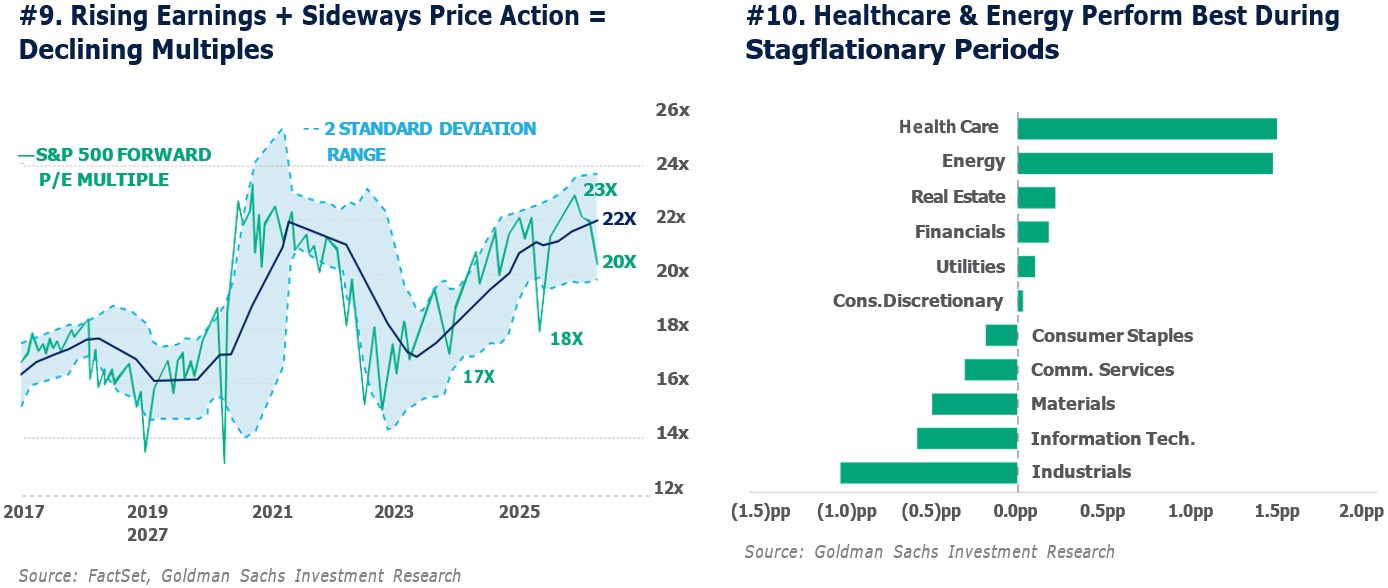

Chart 9 illustrates this clearly: as earnings continue to rise while index performance has remained comparatively subdued, the S&P 500 has become cheaper with a lower multiple. We continue to expect S&P 500 EPS growth in the 11% to 13% range this year, followed by roughly 10% growth in 2027. On that basis, we are maintaining our 7,600 year-end target for the index despite some expected multiple compression. In other words, this is a regime in which fundamentals remain reasonably solid, but further valuation expansion is more difficult to achieve. Markets can still move higher, but future gains will need to be driven increasingly

by earnings growth rather than by multiple re-rating. That said, Chart 10 and Chart 11 both warn against complacency in sector allocation. With valuations across regions and sectors high, cyclicals trading in line with defensives, and global Industrials becoming more expensive than IT, it means that the old cyclical catch-up trade has lost some appeal. A more selec- tive barbell makes sense. Combine areas with direct commodity or defense exposure on one side, and quality secular growers on the other. In practical terms, this means a preference for defense, tradi- tional and alternative energy, utilities, materials, cybersecurity, and hyperscalers.

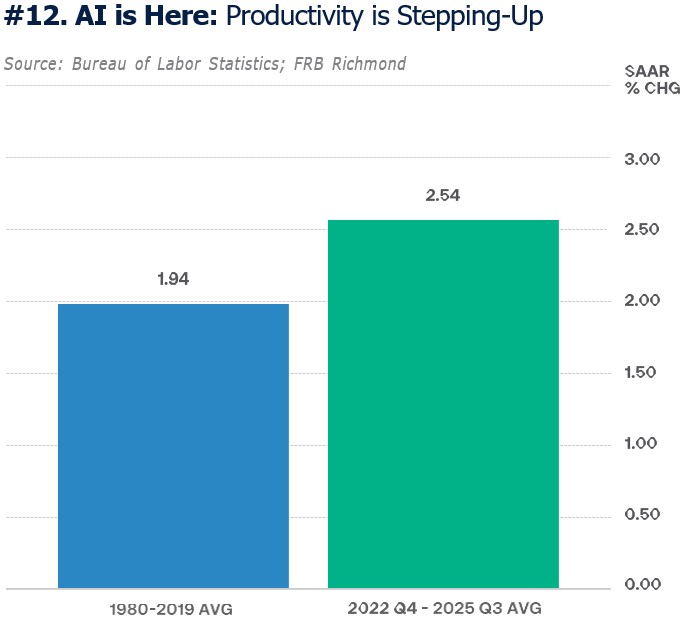

The constructive longer-term case rests above all on Chart 12. This is the most important counter- weight to the geopolitical shock. In our view, AI investment spending and subsequent productivity enhancements should offset the drag from any war-related weakness. The implication is that AI is no longer just a valuation story; it is now feeding through into capex, productivity, and earnings. That does not eliminate short-term volatility, but it does improve the medium-term earnings floor.

The constructive longer-term case rests above all on Chart 12. This is the most important counter- weight to the geopolitical shock. In our view, AI investment spending and subsequent productivity enhancements should offset the drag from any war-related weakness. The implication is that AI is no longer just a valuation story; it is now feeding through into capex, productivity, and earnings. That does not eliminate short-term volatility, but it does improve the medium-term earnings floor.

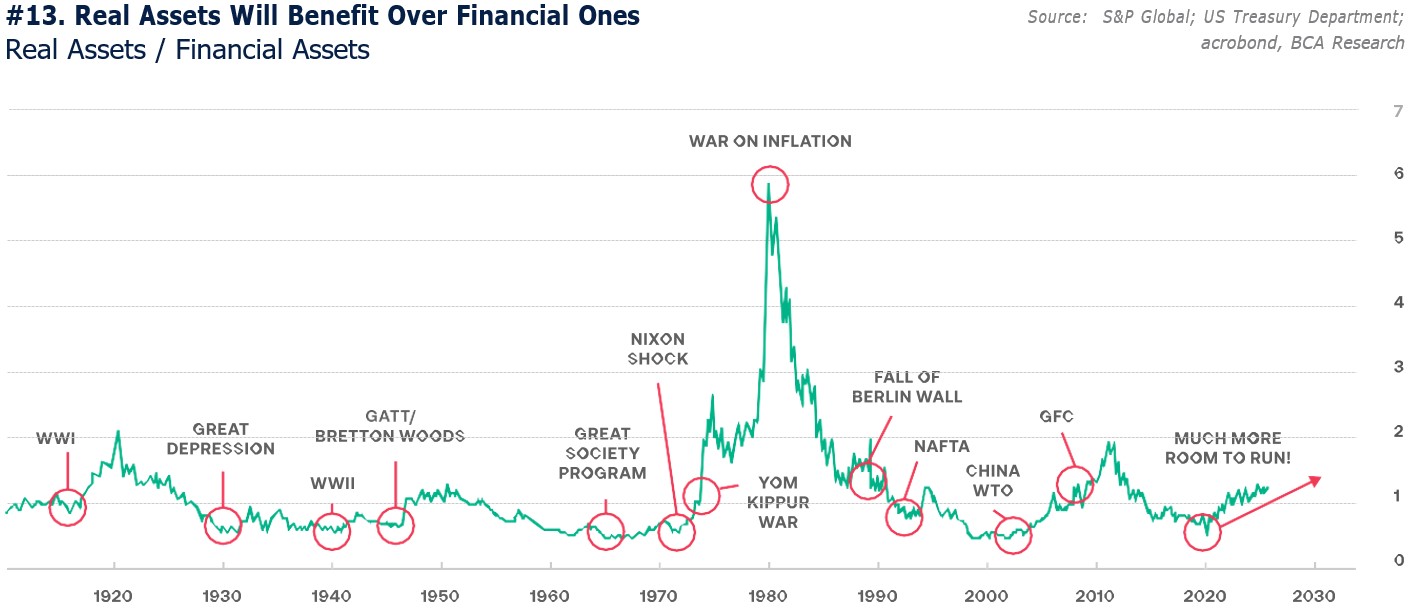

That logic may be extended into portfolio construction, as Chart 13 suggests. If the world is moving into a more fragmented, capital-intensive, security-con- scious phase, then real assets should continue to gain relative standing. This entails rotation toward physical infrastructure, energy security, defense, renewables, and hard assets. That does not mean abandoning financial assets; it means recognizing that the next leg of the cycle may reward businesses tied to power demand, industrial retooling, resource security, and tangible capital formation more than the old duration-heavy winners.

Finally, multipolarity is no longer a thesis; it is the emerging reality. We have argued this for years – including in All Roads Lead to Inflation (Citywire Magazine, June 17, 2020) – but it is now increasingly visible to all market participants. If the world is indeed moving toward a more transactional, sphere-of-influence order, then markets tied to strategic resources, nearshoring, energy, and secu- rity alignment should command greater importance. For Latin America, that may prove more supportive than current headlines suggest, particularly where countries can offer commodities, energy optionality, manufacturing relevance, or geopolitical alignment with a more regionally focused United States. In that

ense, the modern “Donroe Doctrine” is less about coercion than about deeper regional integration, notwithstanding the more forceful rhetoric associ- ated with its namesake.

Putting it all together, our market view is neither complacent nor alarmist. Near-term downside risk remains plausible, as valuations are still elevated, financial conditions have tightened, and the full economic impact of the oil shock has yet to be tested in the hard growth data. But provided Hormuz-related disruptions ease rather than inten- sify, and the region avoids sustained losses in productive capacity, the more constructive under- lying forces should reassert themselves: still-posi- tive global growth, resilient corporate earnings, ongoing AI-led productivity gains, and an expanding opportunity set across real assets and securi- ty-linked themes. In our view, that calls for respecting short-term correction risk without capitulating to it, and for using periods of weakness selectively and strategically.

The late nineteenth century is back – the “Donroe” doctrine: Overall, good news for Latam

When it Rains, it Pours

Geopolitical disruptions from the Iran conflict are extending beyond oil into global logistics and supply chains, but increased resilience from post pandemic adjustments is helping companies absorb shocks while creating new investment opportunities across industries.

Second and third order effects are driving struc- tural shifts across key sectors such as pharma, semiconductors, agriculture, defense, and industrials, accelerating trends like supply chain localization, protectionism, and strategic reconfiguration of global production.

The global renewable energy landscape is splitting in two: U.S. momentum has stalled amid policy shifts favoring fossil fuels and nuclear, while Europe and Asia, especially China, continue expanding renewables in pursuit of energy security.

Despite strong growth in solar, wind, and nuclear in key regions, renewables still face structural constraints, leaving traditional energy sources dominant even as geopolitical shocks, such as the Iran conflict, make the need for diversified power systems a crucial one Global oil and LNG markets have been disrupted by Middle East conflict—especially around the Strait of Hormuz—causing supply interruptions, production shutdowns, and likely higher energy prices for longer.

Production shutdowns can take time to reverse themselves, potentially leading to long-lasting consequences for the global economy, especially for energy-importing countries (particularly in Asia) which are most vulnerable to these shocks.

What does a bomb falling on Kharg Island have to do with the price of everyday goods at Walmart? In today’s global economy, quite a lot. Wars no longer move markets only through immediate macro shocks like oil spikes or falling equities. Instead, they travel quietly through supply chains that connect companies with end clients across continents. Direct shocks to

prices are just the starting point. What follows are second and third order effects, which are the ones that shape global economies. Even if the conflict involving Iran fades from the headlines by the time we publish this article, the following information will serve as a guide on how second and third order effects will reshape industries and economies from now on.

First-order effects are the immediate shocks to pri- ces and inventories. In the case of Iran, this has been reflected directly in oil prices, particularly gi- ven the strategic importance of the Strait of Hormuz for global energy flows. Second-order effects are the transmission of those shocks to end products. For example, everyday goods sold at Walmart become more expensive when oil prices rise, as higher fuel costs increase transportation and logistics expenses across supply chains. Third-order effects emerge as structural adjustments. Once economies absorb the initial shock, they begin adapting to reduce futu- re vulnerability. After Russia’s invasion of Ukraine, for example, many countries faced severe fertilizer shortages. In response, agricultural economies ac- celerated the development of domestic production capacity and sought new international partnerships to reduce dependence on disrupted supply routes. With this in mind, let’s explore how the conflict in Iran will reshape renewables, commodities and other supply chains.

The renewable energy sector is increasingly beco- ming a story of two diverging paths. In the United States, the industry has lost much of its momentum following the passage of the One Big Beautiful Bill, which not only signaled a renewed policy preferen- ce for fossil fuels and internal combustion engine vehicles, but also curtailed support for a range of renewable energy projects. Outside the U.S., howe- ver, many countries continue to push for greater energy independence in the wake of Russia’s inva- sion of Ukraine, even as they struggle with the prac- tical and economic challenges of scaling alternative energy sources. Against this backdrop, and amid the added volatility created by the Iran conflict, it is worth examining how the renewable energy lands- cape is evolving.

Renewable energy in the U.S. has been facing an uphill battle since President Trump took office in 2025, with the President being especially focu- sed on stopping all wind projects and shifting the nation’s power pillars towards hydrocarbons and nuclear power. In this context, it is worth noting that, according to data published by the U.S. De- partment of Energy, renewable sources accounted for more than 20% of total U.S. electricity generation in 2022, with wind representing the largest share. Even so, any renewed momentum for renewables in the U.S. is likely to emerge against a backdrop of rising electricity demand, particularly from data centers. Even if data center construction is facing some opposition in the form of project cancella- tions, demand for wind turbines remains high.

Nuclear energy may prove to be one of the few relative bright spots for clean energy under the Trump administration. According to the World Nuclear Association, the United States is the world’s largest producer of nuclear power, accounting for roughly 30% of global nuclear electricity generation, and it has set targets to quadruple nuclear capacity by 2050. Domestically, nuclear plants generate about 20% of U.S. electricity and nearly 55% of the country’s carbon-free power.

Meanwhile, the other side of the renewable energy story is being shaped by Europe and Asia, parti- cularly China, which is becoming an even more consequential force in the global clean energy market. According to the Economist Intelligence Unit, China is expected to install 276 GW of solar and 84 GW of wind capacity in 2026, accounting for roughly 80% of global solar additions and 78% of global wind additions. Solar power, which is set to remain the fastest-growing source of electricity worldwide, is an area in which China already domi- nates both manufacturing and deployment. EIU pro- jections suggest that China’s total solar capacity could exceed 3,600 GW by 2035 under its updated climate targets. This leadership has also made China one of the world’s leading solar panel exporters, with key markets across Latin America and Asia. Combined with the sharp decline in solar module and cell production costs, this positions China to extend its lead even further across the clean tech- nology landscape. Another segment of the renewable economy in which China is rapidly consolidating its dominance is electric vehicles. According to the In- ternational Energy Agency, Chinese manufacturers now account for more than 70% of global EV pro- duction and roughly 40% of global EV exports. The strength of this trend is equally evident within China’s

domestic market: based on the latest data from the China Passenger Car Association, as reported by The New York Times, about half of all new cars sold in China are either fully electric or hybrid, while roughly one-third of newly sold heavy-duty trucks are fully electric. It is important to note, however, that China’s shift toward renewables does not imply a full retreat from traditional fossil fuels. On the contrary, Beijing’s energy strategy is driven as much by energy security and economic growth as by decarbonization, with the country expanding alternative power sources while maintaining a diversified energy mix. Even so, the direction of travel is becoming clearer. According to forecasts compiled by the EIU, China’s CO2 emissions from fossil fuels peaked in 2025, alongside a decline in demand for refined oil products such as gasoline and diesel. By strengthening its domestic energy base, China is positioning itself to become less vulnerable to external supply shocks, including disruptions like those stemming from the Iran conflict, even if fossil fuels remain part of the mix for years to come.

Europe, for its part, began moving toward greater strategic autonomy from both the U.S. and exter- nal energy suppliers after the outbreak of the Russia-Ukraine war. Yet the continent still imports most of the energy it consumes. As of this year, Europe was importing close to 60% of its energy needs, leaving it heavily exposed, particularly through its dependence on LNG. In that sense, the Iran con- flict may serve as yet another wake-up call for the region. Just as the war in Ukraine prompted a reawakening in European defense spending and domestic industrial capacity, renewed instability in the Middle East is reinforcing the urgency of expanding Europe’s own energy production, in- cluding a faster push into renewables.

To this point, EU energy chief Dan Jørgensen, recently argued that the bloc is in a stronger position than it was in 2022, thanks to a higher share of renewables in

the energy mix and greater system diversification. Additionally, Ursula von der Leyen, President of the European Commission, noted that the share of re- newables in the EU’s electricity mix has surged from 36% in 2021 to nearly 50% now.

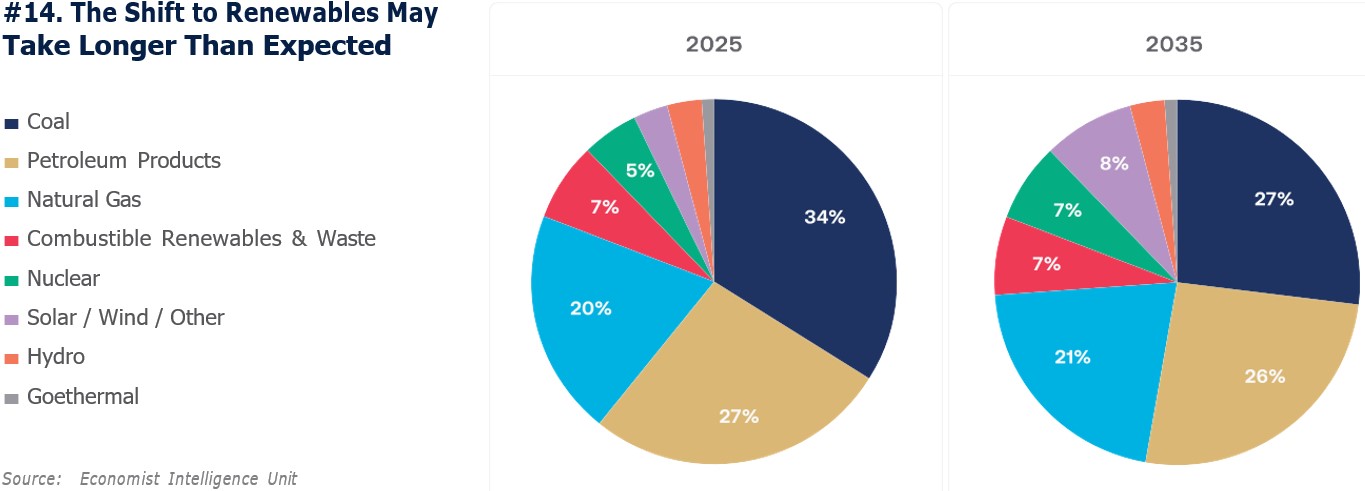

Even though the current backdrop would seem ideal for renewables to assume a more dominant role in global energy supply, they are still expected to remain well behind traditional sources, such as coal and natural gas, as shown in Graph 14. Fur- thermore, the broader operating framework requi- red to support renewables, including grid capacity, system flexibility, and permitting processes, remains a meaningful constraint on the delivery of reliable electricity. Even so, recent conflicts have reinfor- ced a key lesson: energy security depends on di- versification. And if history is any guide, few ca- talysts are as powerful for innovation as necessity – in this case, the growing and urgent need for dependable electricity.

Our relationship with fossil fuels is a fickle one, to say the least. One day we might feel like we are drif- ting apart; the next day we cannot live without them. Take oil, for example. Over the past year, Brent crude prices oscillated between USD 60 and USD 70, ave- raging roughly USD 65, as the world was awash in oil. In fact, after the Covid-19 pandemic, brent crude prices were as low as USD 40. Oil was in decline, as demand projections drifted lower, while supply re- mained ample. That relationship quickly changed over the past month, after the conflict with Iran cur- tailed shipping access through a narrow waterway, merely twenty-three miles wide at its narrowest point, the Strait of Hormuz.

Approximately 20% of global oil supply flows through the Strait of Hormuz; that is one out of every five ba- rrels of oil consumed around the world. More impor- tantly though, the entire Middle East is responsible for producing over one third of the world’s oil, making it the single largest producing region on the planet. Although the Strait is responsible for a deceivingly small amount of flows, the importance of this artery has major implications for global oil markets. Most have heard of global oil production cuts or in- creases in response to expected demand. However, until recently, production shut ins were unheard of.

Think of a production cut or increase as a car driving on the highway that decreases or increases speed. It is easy for a car to change speed as it is moving, but the important thing is that it is still motion. Now think of a production shut in as that same car pulling off to the side of the road and shutting off its engine. The car can still get back on the highway, but since it has stopped moving and actually shut off, it will take more time to get back in the flow of traffic than if it had simply decreased speed. The conflict in the Middle East has caused some of the region’s largest refineries to shut in production, so even if the con- flict ceases tomorrow, it will take time for these refi- neries to bring production back to previous levels. As a result, although oil prices are likely to retreat after the cessation of the conflict, they are likely to remain higher for longer. Additionally, the pre- vious price floor, near USD 40, will likely be reset hi- gher to reflect increased geopolitical tensions, with the lower band of the range likely to rest near USD 60 for the foreseeable future, absent any abnormally large drops in demand.

The ramifications of the conflict start with oil, but they do not end there. The passage through the Strait of Hormuz is equally as important for oil as it is for natural gas, as 20 to 25% of global LNG (Liquefied Natural Gas) exports pass through the same waterway. However, geography matters more for Middle Eastern LNG than for oil. Qatar is by far the single largest producer of LNG in the region. Geographically, this country sits on a small peninsula that stretches out into the Persian Gulf. As a result, unlike oil that can conceivably exit the Middle East in limited quantities trough land-based pipeline systems, the only way for LNG shipments from Qatar to exit the region are via the Persian Gulf, through the Strait of Hormuz, and out into open ocean. So important is this country to the region’s LNG markets, that as this piece was being written, news broke that Iran had attacked the country’s Ras Laffan Industrial City, a complex that houses the world’s largest LNG export

— “The passage through the Strait of Hormuz is equally as important for oil as it is for natural gas, as 20 to 25% of global LNG (Liquefied Natural Gas) exports pass through the same waterway. ”

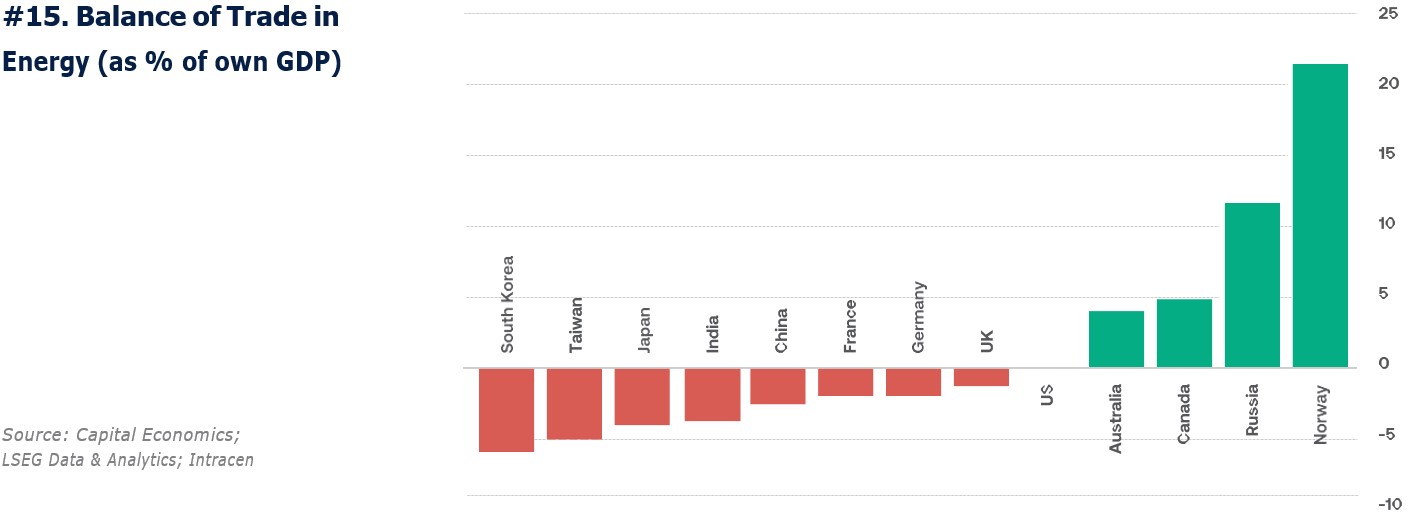

plant, causing extensive damage to the facility, and likely ensuring that LNG prices will remain elevated for longer. Unlike oil, which is used from combustion to feedstock for numerous end products, LNG is almost exclusively used for electrification, heating, and ma- nufacturing. Additionally, the vast majority of LNG is exported to Asia, mainly Japan, South Korea, China, and India, with some of the region’s supply also shipped to Europe. In fact, close to 50% of Japanese and South Korean LNG needs are supplied by the Middle East, while China and India get approximately 30% of their LNG supply from the region. This is important, as countries in Asia are the most likely to be affected by a prolonged conflict and closure of the Strait of Hormuz.

Chart 15 shows a comparison between countries that are net importers and net exporters of energy, mainly oil and gas, to meet domestic needs. As we can see from the chart, the countries that rely hea- vily on imports to meet their domestic energy needs, mainly the Asian countries mentioned above, are going to be the most affected by the current conflict, while the net exporters, on the ri- ght of the chart, will be the least affected. Notice

that the United States lies towards the middle of the chart, slightly on the positive side of the trade ba- lance, as this country is now a net exporter of energy. The difference between net importers and exporters has been reflected by these countries’ respective equity market performance since the conflict began. Case in point, equity markets in most net-exporting countries have retreated between 3-5% since the beginning of the conflict, while those in net-impor- ting nations have pulled back between 10-15%.

But the ramifications do not end there. Further exa- cerbating problems for oil and gas importing na- tions is a strong U.S. Dollar in relation to these na- tions’ currencies. In addition to being a relative safe haven, the USD is intrinsically tied to the oil and gas markets, as global prices in these commodities tend to be quoted in USD, and the commodities are traded in this currency. As a result, a prolonged conflict could temporarily push the U.S. Dollar higher, particularly against other currencies that rely on oil imports, such as the Euro and many Asian currencies.

The current conflict has once again exposed the world’s uneasy dependence on fossil fuels. Just as countries attempt to reduce their reliance on them,

supply disruptions and geopolitical tensions serve as a stark reminder of how essential these energy sources remain and how deeply embedded, they still are in the functioning of economies around the world.

As discussed before, while the most immediate effects of the conflict involving Iran are visible in oil prices, and potentially in a faster transition toward renewable energy, the second and third order effects extend far beyond commodities. In particular, war-related disruptions are already affecting global logistics. Estimates suggest that roughly 10% of the world’s container fleet is currently out of position or delayed, while air strikes have also disrupted parts of Asia’s commercial air routes to Europe. These de- velopments highlight how geopolitical tensions can quickly spill over into the infrastructure that supports global trade.

Should we therefore expect freight rates to rise sharply? Interestingly, not necessarily. One of the structural lessons from both the pandemic and Russia’s inva- sion of Ukraine is that companies have spent the last few years redesigning their logistics networks. By diversifying suppliers, increasing inventories, and building more flexible transportation routes, many firms have developed more resilient supply chains, allowing them to absorb shocks that in the past would have translated directly into higher shipping costs. At the same time, these adjustments are creating opportunities to invest in the industrial transformations that are reshaping global supply chains. Let us explore how some of them may evol- ve in the coming years.

In the pharmaceutical sector, roughly half of all ge- neric prescriptions in the United States are supplied by manufacturers in India, while many of the chemi- cal precursors required to produce those medicines are manufactured in China and often consolidated through logistics hubs in the United Arab Emirates. In addition, several petrochemical inputs used in

— “Chip manufacturing is highly energy intensive, so higher oil prices would directly increase operating costs for fabrication plants across major production hubs such as Taiwan and South Korea”

drug manufacturing depend heavily on supplies from the Persian Gulf. Generic drugs are particularly vulnerable because they operate with the lowest margins in the pharmaceutical industry, leaving little room to absorb higher input or transportation costs.

With companies typically maintaining only 30 to 60 days of inventory, a prolonged disruption could eventually ripple through the U.S. healthcare sys- tem, affecting the availability and pricing of essen- tial medicines. As a potential third-order effect, sus- tained disruptions could accelerate efforts by governments and pharmaceutical companies to reshore parts of the supply chain, diversify che- mical sourcing, and invest in domestic produc- tion capacity for critical medicines.

Apparel is another industry already feeling the effects of war. Much of the world’s fast-fashion production is concentrated in Pakistan, India, and Bangladesh, with a significant share of shipments moving through routes connected to the Persian Gulf. As a result, companies that rely heavily on these supply chains could see pressure on their business models if transportation becomes more complex or delayed. At the same time, this disruption may create oppor- tunities for other emerging-market economies with competitive labor costs to capture part of the supply chain, as global brands diversify production and build more geographically balanced inventories.

Semiconductors could also face meaningful pres- sure from disruptions around the Strait of Hormuz. Chip manufacturing is highly energy intensive, so higher oil prices would directly increase operating costs for fabrication plants across major production hubs such as Taiwan and South Korea. At the same time, the industry depends on a complex web of inputs including petrochemicals, specialty chemicals, and industrial gases, meaning disruptions could affect not only transportation and energy costs but also critical materials such as helium. For instance, Qatar accounts for roughly 40% of global helium production. As a third order effect, persistent geopolitical risk could reinforce the strategic push by governments to localize and diversify semiconductor supply chains, a trend already underway through policies such as the CHIPS and Science Act in the United States.

Agriculture and food production are likely to be among the sectors most severely affected, particularly through disruptions to fertilizer supply. According to the American Farm Bureau Federation, countries exposed to the conflict in the region account for roughly 30% of global ammonia exports and nearly 49% of global Urea exports, two essential compo- nents in the production of modern nitrogen fertilizers. Major exporters such as Saudi Arabia, Qatar, and Russia benefit from access to very cheap fossil fuels, particularly LNG, which can represent close to 80% of fertilizers’ production costs. This leaves large agricultural-based economies exposed. Brazil, for example, imports roughly 85% of its fertilizer needs. Therefore, these disruptions could push food prices higher by compressing farm yields and increasing production costs, adding pressure to global inflation. Farmers may also adjust planting decisions in response to higher fertilizer prices, shif- ting away from nitrogen intensive crops such as Corn toward crops like Soybeans, which naturally fix nitrogen in the soil. Over the longer term, these shocks are likely to reinforce calls for greater agri- cultural protectionist policies, as the major conflicts of the past five years have exposed how vulnerable global food systems are to conflict.

On the other hand, Aerospace and Defense have emerged as one of the clearest structural beneficiaries of the current geopolitical environment, as govern- ments continue to increase military spending in res- ponse to rising security risks. Defense companies in South Korea, for example, are reporting record order books and strong export momentum, su- pported by growing demand from NATO members and countries across the Middle East. In Europe, the conflict in Ukraine reinforced the urgency to re- build depleted military inventories while accelerating efforts to expand domestic defense capabilities and reduce reliance on the United States for security and weapons systems.

Finally, Industrial materials could also face important second and third order effects from disruptions linked to the Strait of Hormuz. In the near term, higher energy prices associated with tensions involving Iran raise production costs for energy intensive ma- terials such as steel, aluminum, and cement, while higher fuel prices increase transportation costs across construction and manufacturing supply chains. Over time, these pressures may lead to structural adjustments, as companies relocate energy intensive production to regions with cheaper and more stable energy sources, particularly in North America, where abundant natural gas and expanding renewable ca- pacity provide a cost advantage.

While we could spend days discussing the ways in which the events unfolding in Iran may affect daily life, Table 1 highlights several of the key sectors where meaningful medium-term structural shifts and investment opportunities are likely to emerge. From energy to food, disruptions tied to the Strait of Hormuz extend well beyond oil markets, creating ripple effects across the global economy and ope- ning new areas of investment interest. As supply chains adapt to the risks surrounding Iran, the- mes such as protectionism, supply chain locali- zation, and technologies designed to reduce strategic vulnerabilities are likely to play an increa- singly important role in portfolio positioning over the years ahead. In the end, geopolitical choke- point disruptions can accelerate fragmentation, rerou- ting, resilience-building, and technology adoption across trade and logistics systems.

Important Disclosures

Insigneo Financial Group, LLC comprises a number of operating businesses engaged in the offering of brokerage and advisory products and services in various jurisdictions. Brokerage products and services are offered through Insigneo Securities, LLC, a broker-dealer registered with the U.S. Securities and Exchange Commission (“SEC”) and member of FINRA and SIPC. Investment advisory products and services are offered through Insigneo Advisory Services, LLC, an investment adviser registered with the SEC. Insigneo has affiliated companies in different locations, so it is important to understand which entity you are conducting business with. Please visit https://insigneo.com/legalentities/ for more information about the differences between these companies, their locations, and what that means for you.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security. It is for general information purposes only. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to securities, those references do not constitute a recommendation to buy, sell or hold such security. It does not constitute a recommendation or a statement of opinion, or a report of either of those things and does not, and is not intended, to consider the particular investment objectives, financial conditions, or needs of individual investors. Any target prices provide reflect our current expectations, are subject to change and may not be achieved due to a variety of risks, including changes in economic conditions, interest rates, geopolitical developments, and issuer-specific factors. The target price does not guarantee future results and should not be relied upon as a sole basis for investment decisions.

Not All Risks Are Disclosed – Past performance is not indicative of futures results. Investments involve significant risks, and it is possible to lose some or all of your principal investments and therefore may not be suitable for everyone. Always consider whether any investment is suitable for your particular circumstances and, if necessary, seek professional advice from your Investment Professional. This material may contain opinions, expressions, and estimates that represent the analysis and perspective of Insigneo Securities, LLC’s Investment Strategy department or its providers at the time of publication. These are subject to change at any time, without notice.

FOR AFFILIATES LOCATED IN CHILE

Insigneo Asesorías Financieras SPA se encuentra inscrito en Chile, en el Registro de Prestadores de Servicios Financieros de la Comisión para el Mercado Financiero. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de emisión de este. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera.

Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Asesorías Financieras SPA ni ninguna de sus empresas relacionadas.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta o solicitud de compra o venta de ningún valor en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en cuentas de corretaje y de asesoramiento de inversiones están sujetas al riesgo de mercado, incluida la pérdida de capital.

La información base del presente informe puede sufrir cambios, no teniendo Insigneo Securities LLC ni Insigneo Asesorías Financieras SPA la

obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.

FOR AFFILIATES LOCATED IN URUGUAY

Insigneo Asesor Uruguay S.A. está inscripto en el Registro de Mercado de Valores del Banco Central del Uruguay como Asesor de Inversiones. En Uruguay, los valores están siendo ofrecidos en forma privada de acuerdo al artículo 2 de la ley 18.627 y sus modificaciones. Los valores no han sido ni serán registrados ante el Banco Central del Uruguay para oferta pública. Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted según su perfil y estrategia de inversión. Este documento no constituye un asesoramiento ni una recomendación u oferta o solicitud de compra o. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso. Rentabilidades históricas de los productos anunciados no aseguran rentabilidades futuras..

FOR AFFILIATES LOCATED IN ARGENTINA

Insigneo Argentina S.A.U. Agente Asesor Global de Inversión se encuentra registrado bajo el N° 1053 de la Comisión Nacional de Valores (CNV) e inscripto ante la Inspección General de Justicia (IGJ) bajo el N° 12.278 del Libro 90, Tomo –, de Sociedades por Acciones. Este informe fue efectuado por área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, en base a la información disponible a la fecha de su emisión. Para evitar cualquier conflicto de interés, Insigneo Securities LLC dispone que ningún integrante del equipo de Research & Strategy tenga su remuneración asociada directa o indirectamente con una recomendación o reporte específico o con el resultado de una cartera. Aunque los antecedentes sobre los cuales ha sido elaborado este informe fueron obtenidos de fuentes consideradas confiables, no podemos garantizar la completa exactitud e integridad de estos, no asumiendo responsabilidad alguna al respecto Insigneo Securities LLC, Insigneo Argentina S.A.U. ni ninguna de sus empresas relacionadas. La información base del presente informe puede sufrir cambios, no teniendo Insigneo Argentina S.A.U. la obligación de actualizar el presente informe ni de comunicar a sus destinatarios sobre la ocurrencia de tales cambios.

Este material está destinado únicamente a facilitar el debate general y no pretende ser fuente de ninguna recomendación específica para una persona concreta. Por favor, consulte con su ejecutivo de cuentas o con su asesor financiero si alguna de las recomendaciones específicas que se hacen en este documento es adecuada para usted. Este documento no constituye una oferta, recomendación o solicitud de compra o venta de ningún valor negociable en ninguna jurisdicción en la que dicha oferta o solicitud no esté autorizada o a ninguna persona a la que sea ilegal hacer dicha oferta o solicitud. Las inversiones en valores negociables están sujetas al riesgo de mercado, incluida la pérdida parcial o total del capital invertido. Cualquier opinión, expresión, estimación y/o recomendación contenida en este informe constituyen el juicio o visión de área de Research & Strategy de Insigneo Securities LLC. o sus proveedores, a la fecha de su publicación y pueden ser modificadas sin previo aviso.